Alison Okatch

June 29, 2026

Share article

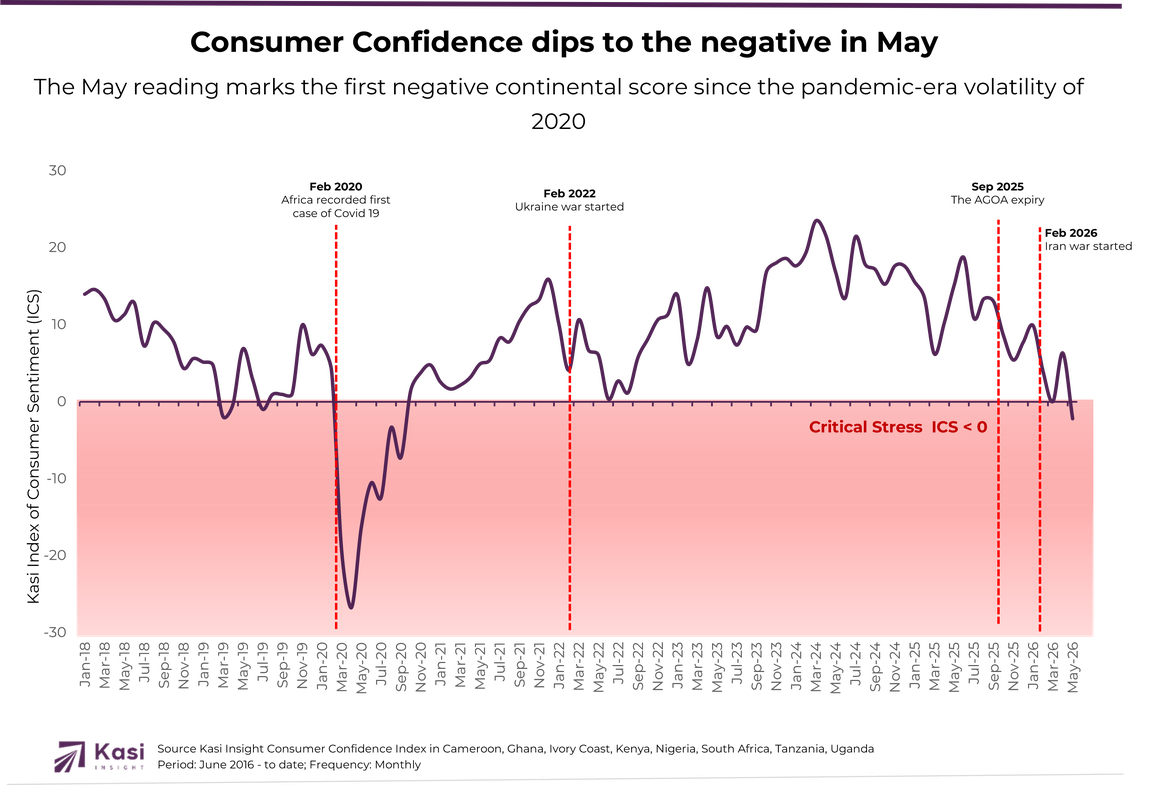

After nearly three years of remaining largely in positive territory, Africa's Consumer Confidence Index fell to -2.2 in May 2026, signalling a renewed deterioration in consumer sentiment across the continent.

While the decline may appear modest, it is symbolically significant. The May reading marks the first negative continental score since the pandemic-era volatility of 2020 and suggests that consumers are becoming increasingly cautious about their economic prospects.

The latest Kasi Index of Consumer Sentiment (ICS) suggests that Africa is increasingly splitting into three distinct consumer realities. This average conceals stark differences between countries. Some consumers are regaining confidence (Recovery Markets), others remain remarkably resilient despite economic pressures (Resilient Optimist), and a third group is showing signs of deep strain (Strained Markets).

The result is an Africa that can no longer be understood through a single consumer lens.

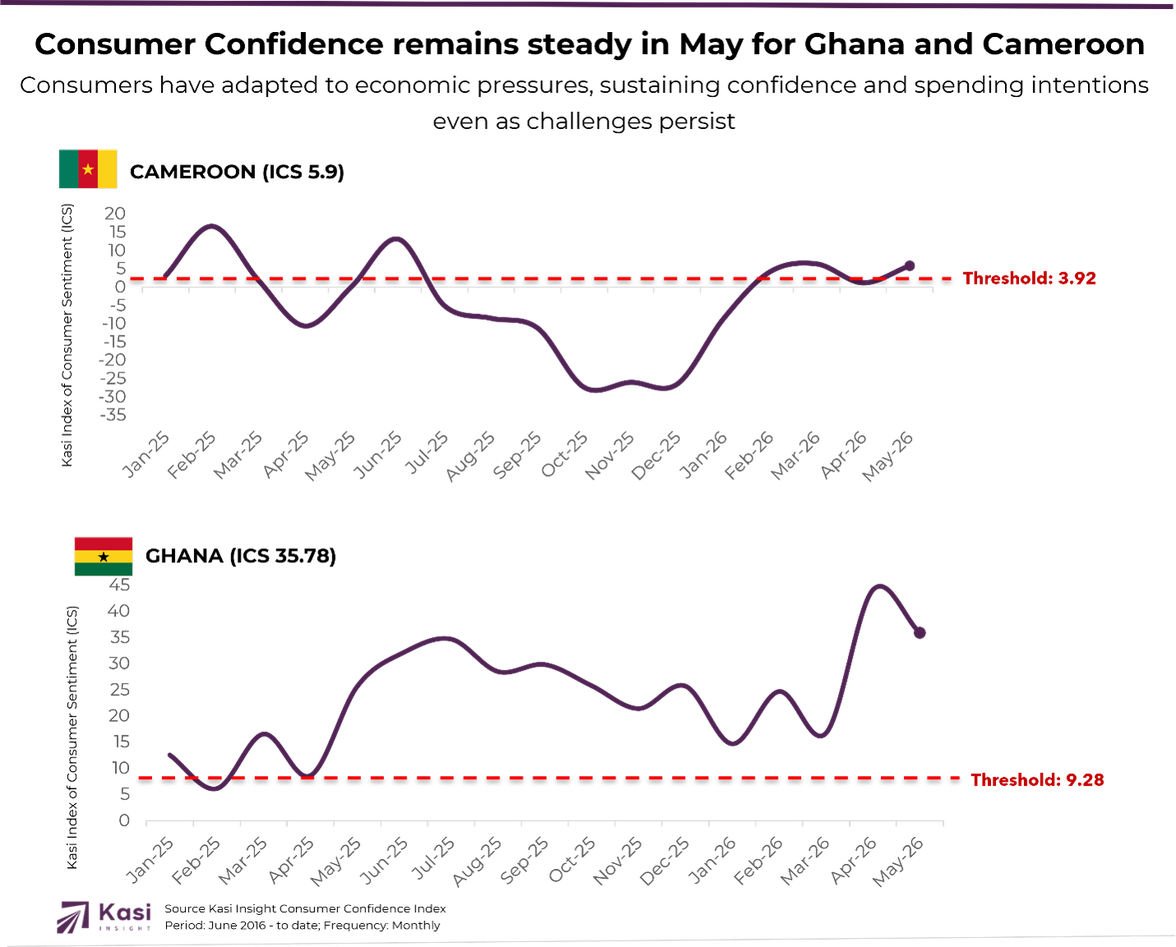

Resilient markets are defined not by recovery, but by consumers' ability to maintain confidence despite continued economic headwinds

In a period when several African markets remain under pressure and the continental average has slipped into negative territory, consumers in Ghana and Cameroon, are increasingly looking forward rather than backward.

Ghana ICS after fluctuating through 2024 and early 2025, sentiment accelerated sharply in 2026, rising from 14.7 in January to 44.1 in April before settling at 35.9 in May. The significance is not simply the score itself. Ghana now consistently ranks among the most optimistic consumer markets in Africa. The market may therefore be entering a phase where growth is driven not only by necessity spending but also by renewed consumer aspirations.

Cameroon throughout the second half of 2025, sentiment deteriorated significantly, falling to -26.5 in December 2025. Such readings typically indicate widespread consumer caution and reduced willingness to spend. By early 2026, consumer sentiment rebounded sharply from -8.6 in January to positive territory, remaining resilient through H1 2026 to May (+5.9) despite some month-to-month volatility.

Rather than focusing solely on helping consumers cope with economic pressures, brands can begin tapping into ambition, lifestyle upgrades, and discretionary spending occasions.

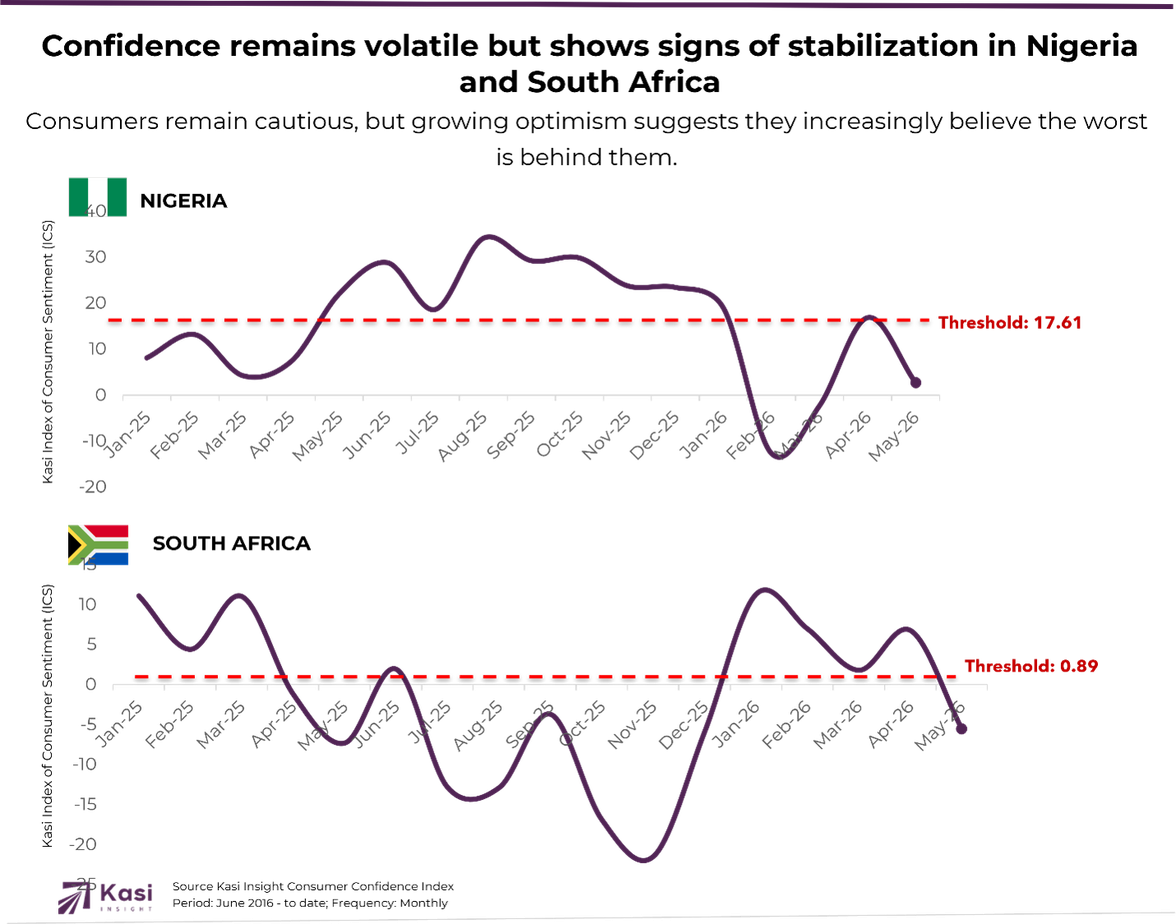

The defining characteristic of these markets is not strong confidence, but cautious stabilization.

South Africa and Nigeria illustrate a consumer reality that sits between recovery and strain. In both markets, confidence remains highly sensitive to economic developments, resulting in periodic swings between optimism and caution.

Yet despite this volatility, there are signs that consumers are beginning to stabilize their expectations. Rather than experiencing the sharp collapses seen during previous crises, households appear to be adapting to a new economic normal.

South Africa’s consumer confidence has recovered significantly from the deep pessimism seen between 2022 and 2025. After improving from -21.5 in November 2025 to -5.9 in December, sentiment turned positive in early 2026, peaking at 11.3 in January before moderating and slipping back to -5.5 in May. Despite this setback, the overall trend points to a more stable and less pessimistic consumer environment.

Nigeria’s consumer confidence remains positive but has become increasingly volatile in 2026, falling from 18.9 in January to -12.7 in February before recovering to 2.7 in May. While optimism has softened from previous highs, consumers have not shifted into sustained pessimism, reflecting continued sensitivity to changing economic conditions.

Success will depend on reducing perceived risk for consumers and giving them confidence to spend rather than simply persuading them to spend.

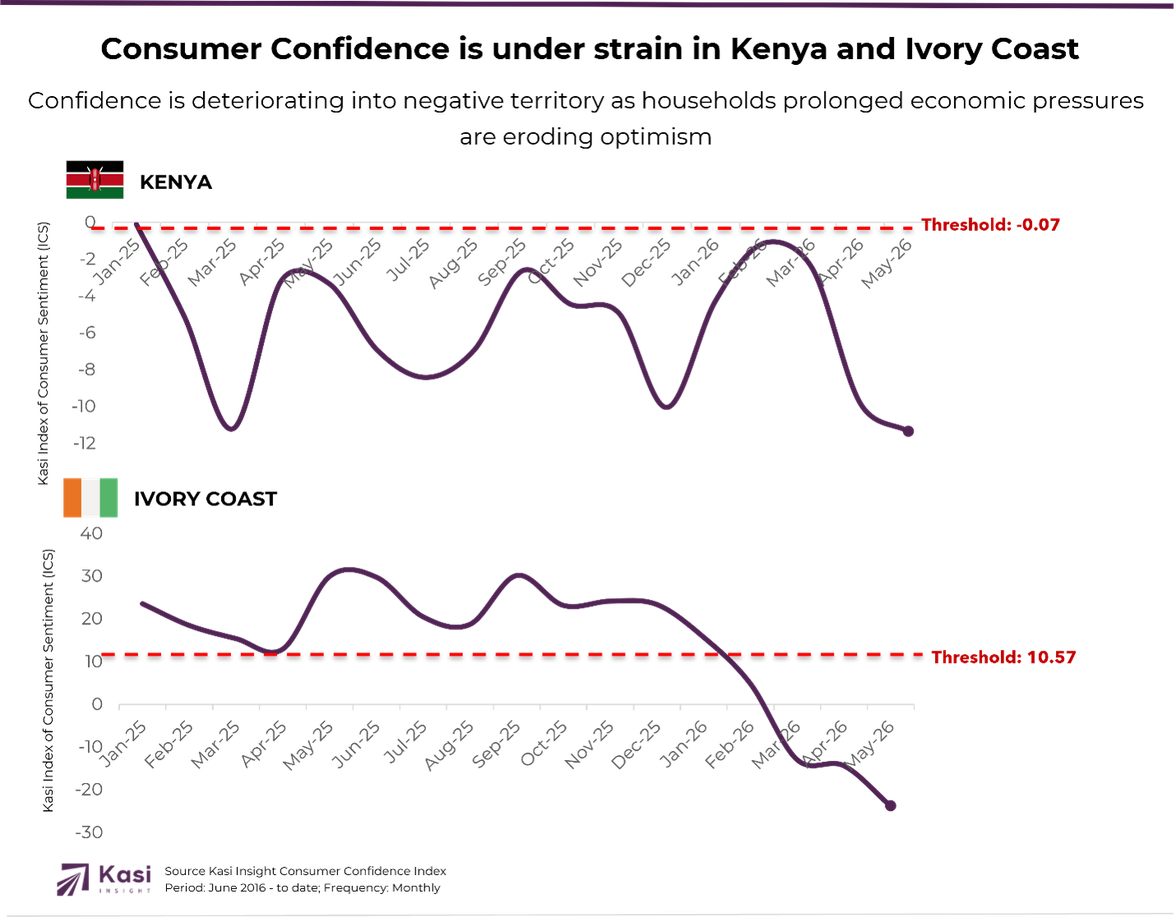

The defining characteristic of strained markets is not simply low confidence, but the growing disconnects between consumer aspirations and economic reality.

Kenya and Ivory Coast stand out as the clearest examples of strained consumer markets. In both countries, consumer confidence has moved decisively into negative territory, signalling growing concerns about household finances, spending power, and the broader economic outlook. The result is a consumer environment characterized by restrained spending, heightened price sensitivity, and limited confidence in the near-term future.

Ivory Coast has seen one of the sharpest sentiment reversals in the dataset, shifting from one of Africa’s most optimistic markets in 2024–2025, with confidence consistently above 20 points, to the weakest in 2026. Sentiment fell from 15.8 in January to -23.8 in May, highlighting a rapid transition from optimism to deep consumer caution.

Kenya’s consumer confidence story is defined by persistent pessimism rather than a sharp decline. Sentiment remained negative throughout 2025 and 2026, moving from -10.0 in December 2025 to -11.3 in May 2026 after only a brief improvement early in the year. This sustained weakness suggests consumer caution has become entrenched, limiting the prospects for a meaningful recovery.

In these environments, consumers are actively reassessing every purchase, making affordability and utility critical competitive advantages.

As consumer sentiment fragments, businesses must align their growth, pricing, innovation, and communication strategies to the specific consumer reality within each market.

Africa is no longer a single consumer story. The continent is simultaneously home to consumers who are rebuilding confidence, cautiously stabilizing, and becoming increasingly constrained. Winning brands will be those that move beyond continent-wide assumptions and tailor their strategies to the specific consumer reality of each market.

To summarize;

Resilient Optimists (Ghana, Cameroon) require inspiration; Aspirational products, innovation, premium tiers, and messaging centered on progress, achievement, and opportunity.

Recovery Markets (South Africa, Nigeria) require reassurance. Flexible pricing, smaller pack sizes, loyalty programs, financing options, and communications that emphasize reassurance, stability, and tangible value.

Strained Markets (Kenya, Ivory Coast) require affordability. Value propositions, affordable formats, promotions, budget-friendly innovations, and messaging focused on practicality, savings, and helping consumers navigate economic pressure.

As consumer confidence fragments across Africa, the winners will be those who can see these shifts first. The Kasi Consumer Sentiment Index helps businesses move beyond assumptions and respond to the realities shaping consumer behavior in each market.

Kasi Insight is Africa's leading decision intelligence firm specializing in high-frequency consumer and economic data across Africa. Through its proprietary survey infrastructure and analytics platform, Kasi provides real-time insights that help organizations anticipate economic shifts, understand consumer behavior, and make better strategic decisions.

We welcome collaboration with:

Organizations interested in exploring partnerships or accessing Kasi datasets are invited to contact our research team.

📧 yannick@kasiinsight.com

9 views

Share article

H1 2026 exposed the rise of the optimisation economy, with consumers actively reallocating spending rather than simply cutting back.

African consumers have shifted from pursuing wealth to pursuing financial resilience, creating a new expectation that banks should help them build financial wellbeing

Assessment Of the Potential for Trade and Investment Exchanges Between Quebec and Africa