Sandra Beldine Otieno, MSc

July 11, 2025

Share article

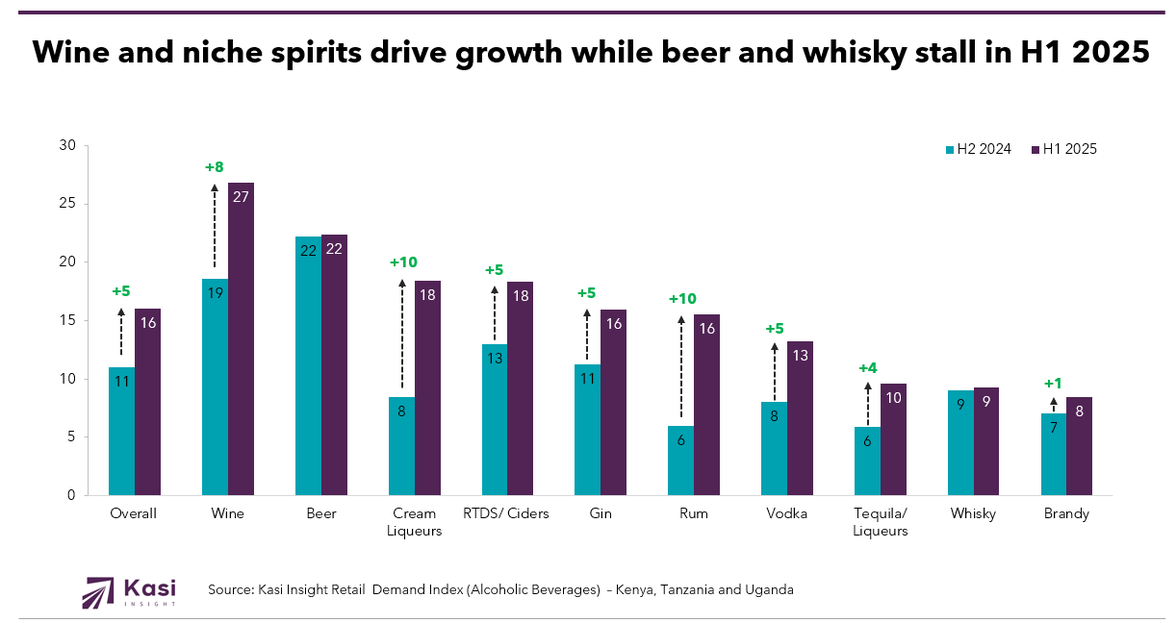

Alcohol consumption in East Africa is entering a period of rapid transformation. In the first half of 2025, consumers in Kenya, Uganda, and Tanzania signaled that their tastes and spending priorities are evolving faster than many brands anticipated. From cream liqueurs and rum to ready-to-drink ciders and wine, more diverse preferences are reshaping purchasing decisions, while traditional staples like beer and mainstream spirits face growing competition. According to Kasi Insight’s Retail Demand Index, measured quarterly on a scale from +100 to −100, growth is no longer uniform across categories or countries.

Between the second half of 2024 and the first half of 2025, the overall demand for alcohol in East Africa increased by 5 points, rising from 11 to 16. This steady improvement reflects a growing openness to experimenting beyond familiar options. Cream liqueurs and rum posted the largest gains, each adding 10 points over the period. Wine advanced by 8 points to reach an index of 27, confirming that consumers increasingly associate it with special occasions and affordable luxury.

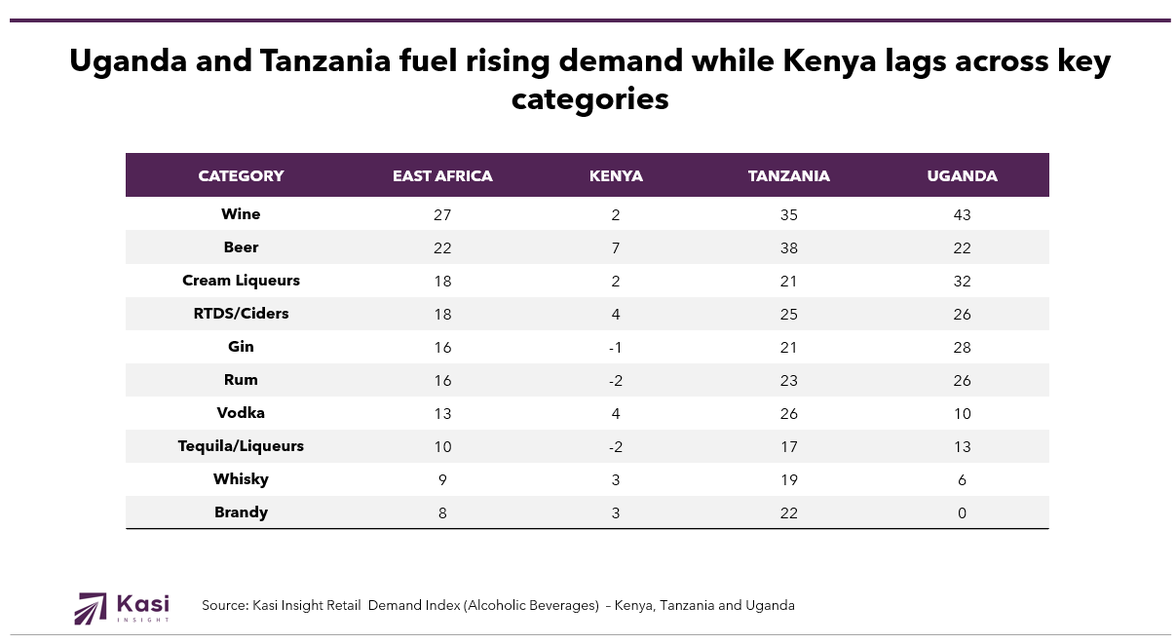

Wine’s performance stands out most clearly in Uganda and Tanzania. In Uganda, wine demand reached an index of 43, underscoring its role as a symbol of status and personal indulgence among middle- and upper-income consumers. Tanzania followed closely with an index of 35, reflecting a shift away from beer and mainstream spirits toward products perceived as more sophisticated. This pattern suggests that wine has moved beyond its niche origins to become a mainstream choice for consumers seeking refined experiences without fully entering the high-end spirits segment.

Ready-to-drink ciders, gin, and vodka also recorded steady improvements, each gaining between 4 and 5 points. These categories highlight the growing importance of convenience and novelty in purchasing decisions. In contrast, beer showed no change in demand, ending the period with an index of 22, while whisky remained flat at 9. Brandy and tequila posted only modest increases, indicating that while they retain steady followings, they have not broken into broader popularity.

While the regional story points to moderate growth, the country-level trends are more revealing. Tanzania emerged as the most dynamic market in the region, with its overall demand increasing by 9 points over the period. Consumers in Tanzania are showing strong appetite across nearly every category, particularly wine, which reached an index of 35, and beer, which climbed to 38. This broad-based growth suggests that both every day and premium consumption occasions are expanding.

Uganda also recorded strong momentum, with a 5-point rise in overall demand. Wine demand reached an index of 43, the highest single score observed in any category across the three countries. Cream liqueurs, gin, and ciders all posted high indices as well, demonstrating that Uganda’s consumers are becoming more open to diverse drinking experiences and more willing to invest in perceived quality.

In contrast, Kenya was the only market where overall demand declined, falling by 4 points over the same period. Several key categories ended in negative territory, with gin at –1, rum at –2, and tequila at –2. Even wine, which showed strength elsewhere, registered an index of only 2. Vodka and whisky posted modest gains, but these were not enough to offset the broader softness. The data suggest that inflation, tighter household budgets, or regulatory changes may be weighing on confidence and purchasing power in Kenya.

These contrasting trajectories highlight a market no longer defined by a single trend. In Tanzania, the expansion of both accessible staples and indulgent categories suggests a dual mindset: consumers are embracing variety and blending affordable options with aspirational choices. Uganda has emerged as a frontier for premium experimentation, with urban consumers increasingly willing to trade up for richer, more diverse products. In Kenya, the decline in demand underscores how quickly discretionary spending can stall when confidence erodes.

This signals that traditional strategies anchored in beer or mainstream spirits are unlikely to capture the next wave of growth. The rise of categories like cream liqueurs, rum, and ciders shows that consumers expect both novelty and clear value. Meanwhile, the divergence between countries reinforces that a uniform approach will likely miss critical opportunities shaped by local economic and cultural dynamics.

These shifts create both challenge and opportunity for producers, distributors, and retailers as they plan for the second half of the year. In Uganda and Tanzania, the priority will be to build on strong momentum in premium categories. Brands that invest in storytelling, education, and sampling can deepen consumer understanding of wine and cream liqueurs. These products have moved beyond novelty into symbols of taste and aspiration, and there is clear potential to turn occasional buyers into regular customers through targeted experiences and promotions.

In Kenya, the focus will need to be on defending market share in an environment defined by caution. As consumers become more price sensitive, producers can explore pack size innovation and entry-level variants to maintain relevance. At the same time, messaging that emphasizes value and quality reassurance will help rebuild confidence. Even in a market under pressure, there are segments willing to spend if products feel accessible and worth the investment.

Across the region, the most important consideration is that segmentation has become the primary engine of growth. Brands that treat East Africa as one homogenous market risk missing the nuanced shifts happening within each country. Data-driven strategies that track demand by income, age, and lifestyle will be essential to capture new pockets of growth and respond quickly when tastes change. As the second half of 2025 unfolds, producers who act on these insights will be better positioned to secure share and shape the future of the region’s alcohol market.

Share on socials using this caption: 🍷📈 In H1 2025, East Africa’s alcohol demand split in new directions. Wine, cream liqueurs, and rum surged while beer and whisky held steady. Uganda and Tanzania led the way, but Kenya showed slower growth. Explore the trends driving this shift and see how segmentation is reshaping the market. #EastAfrica #AlcoholTrends #ConsumerInsights #2025Growth

2288 views

Share article

Cameroon’s protein market in 2026 is shifting from habitual consumption to structured and intentional demand

Consumer Choices Post COVID-19 Are Redefining Kenya’s Beverage Landscape

Nigeria’s alcoholic beverages market shows resilience in beer but steep H1 declines in premium categories