Sandra Beldine Otieno, MSc

August 23, 2024

Share article

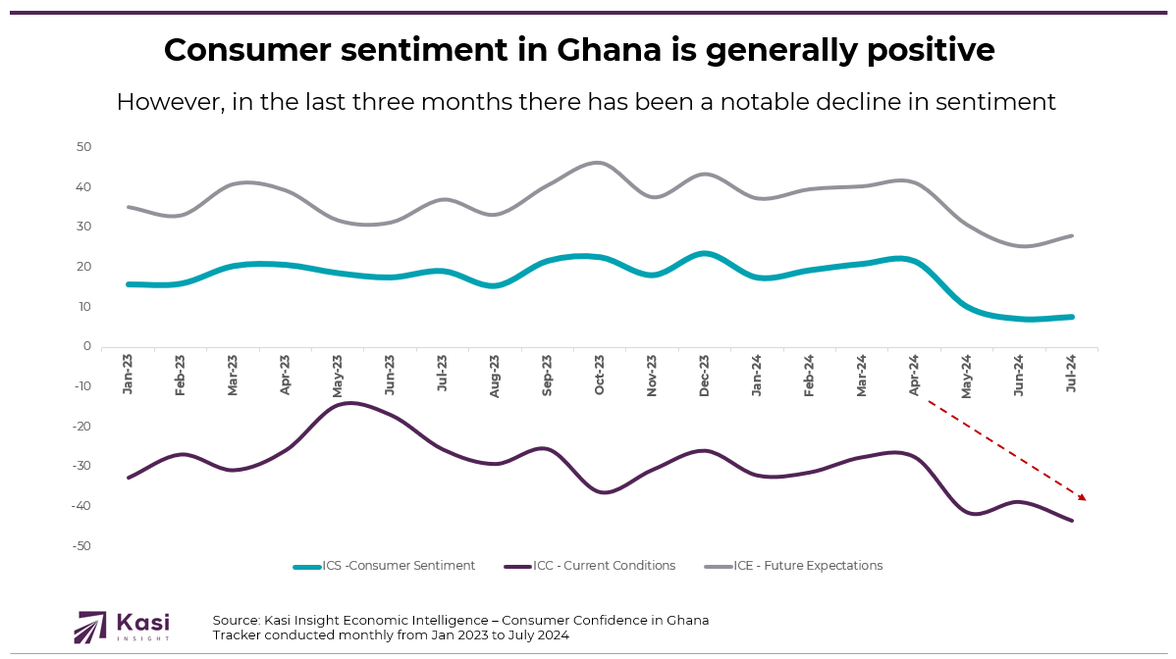

The Index of Consumer Sentiment (ICS) from Kasi Insight, which monitors economic perceptions in Ghana from January 2023 to July 2024, shows that consumer confidence remained generally positive throughout this period. In 2023, the ICS gradually rose from 16 in January to a high of 24 in December, suggesting a cautiously optimistic outlook among Ghanaians, likely bolstered by positive economic developments and stabilizing policy measures. Despite this positive sentiment, the Index of Current Conditions (ICC) stayed negative, never exceeding -14, indicating that while consumers felt optimistic, they were still grappling with challenges such as inflation and unemployment that affected their day-to-day lives.

However, a notable shift occurred in 2024. While the ICS maintained a generally positive stance through April, it experienced a significant decline in the last three months, dropping from 22 in April to 10 in May 7 in June, and recovering slightly to 8 in July. This sharp decline in the ICS, despite remaining in positive territory, suggests a rising concern among consumers about emerging economic challenges or uncertainties. Similarly, the Future Expectations Index (ICE), which had reached a high of 46 in October 2023, also fell sharply in 2024, dropping from 31 in May to 25 in June, with a modest recovery to 28 in July. These declines highlight heightened consumer apprehension about Ghana's economic future, underscoring a fragile sentiment amidst evolving global and local economic pressures.

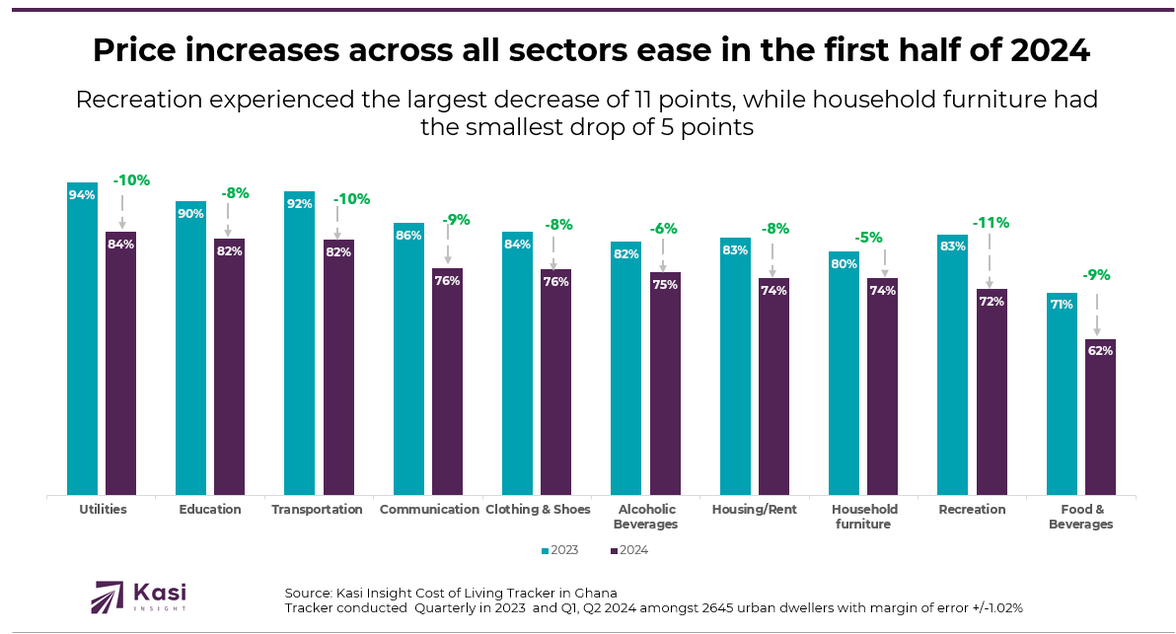

Kasi Insight’s Cost of Living Tracker, which assesses the impact of rising costs on consumers and their coping strategies, highlights significant shifts in how Ghanaian consumers perceive price increases across various sectors in the first half of 2024. In 2023, perceptions of price hikes were notably high across all categories. For instance, 94% of consumers reported an increase in utility costs in 2023, which declined to 84% in early 2024, reflecting a 10% decrease. Similar trends were observed in other essential sectors, including transportation and food & beverages, where perceived price increases fell by 10% and 9%, respectively.

Recreational activities experienced the largest decline in perceived price increases, dropping from 83% in 2023 to 72% in the first half of 2024, indicating an 11% decrease. This trend could suggest price stabilization within the recreational sector or a reduction in spending due to economic pressures, leading to a lower sensitivity to price changes. Similarly, sectors essential for daily living, such as housing, clothing, and education, saw an 8% decrease in perceived price hikes. These changes reflect a potential easing of price pressures or an adjustment in consumer expectations following a period of high inflation. The data indicates a broader trend of reduced perceptions of inflationary pressures, which could influence consumer confidence and spending behavior moving forward.

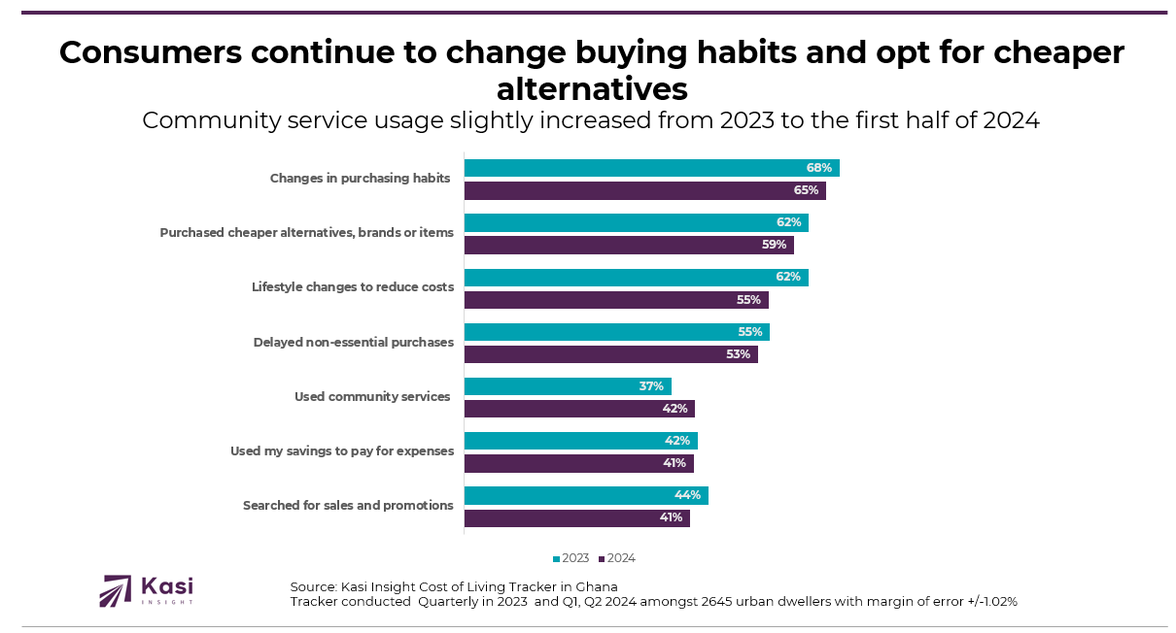

Consumer adaptation strategies in Ghana during the first half of 2024 reveal some key shifts. In 2023, 68% of consumers reported changes in their purchasing habits, which slightly decreased to 65% by mid-2024. This small decline suggests that adaptation strategies might be stabilizing, or consumers may have reached a limit in adjusting their buying behaviors. The use of cheaper alternatives or brands also saw a modest drop, from 62% in 2023 to 59% in early 2024, indicating a reduced urgency to switch, potentially due to a saturation of available cheaper options or changing price perceptions. Similarly, lifestyle changes aimed at reducing costs declined from 62% to 55%, showing that while such changes are still significant, fewer consumers felt the need to drastically alter their daily habits compared to the previous year.

Conversely, reliance on community services grew, increasing from 37% in 2023 to 42% in the first half of 2024. This rise suggests a greater dependence on community-based solutions as a cushion against economic challenges, reflecting increased community engagement or availability of such services. The percentage of consumers using their savings to cover expenses remained stable, slightly dropping from 42% to 41%, indicating a continued reliance on savings as a financial strategy amid rising costs. Meanwhile, the search for sales and promotions declined from 44% in 2023 to 41% in 2024, possibly pointing to a reduced perceived value or availability of such deals or consumer fatigue from constantly seeking discounts as a long-term coping strategy.

In Ghana's evolving consumer market through the first half of 2024, the dynamics between value and premium brands are subtly shifting. Although the preference for cheaper alternatives has slightly decreased from 62% in 2023 to 59% in early 2024, value brands continue to hold significant appeal. This trend suggests a market nearing saturation yet still receptive to brands that consistently offer clear value and innovation. The stabilization in consumer behavior adjustments indicates that the explosive growth in demand for value brands may level off, yet it doesn't signal a decline. For premium brands, the economic landscape is mixed. Despite ongoing uncertainties and a downturn in economic optimism, the easing of perceived price pressures and less concern about inflation could slowly enhance the attractiveness of premium offerings, particularly for consumers whose financial situations remain stable, viewing these products as worthwhile investments or occasional luxuries.

The rising utilization of community services, from 37% in 2023 to 42% in 2024, and stable savings habits reflect a consumer base increasingly relying on creative and communal solutions to financial pressures. This scenario provides an opportunity for premium brands to forge deeper community ties and develop loyalty programs that reinforce their value beyond price points. Meanwhile, the decline in enthusiasm for sales and promotions suggests a shift in consumer engagement strategies. Both value and premium brands might need to look beyond traditional discounting, focusing instead on enhancing product distinctiveness and customer experience. This approach could more effectively meet the evolving expectations of Ghanaian consumers, aligning with a market that values both economic pragmatism and quality.

Share on socials using this caption: 📉 Ghana's Consumer Sentiment Remains Positive but Cautious! 📊 Despite easing inflation, recent months show a dip in confidence as Ghanaians adapt by changing spending habits and seeking more affordable options. 💸💼 #GhanaEconomy #ConsumerTrends #Outlook

2060 views

Share article

From Price Shock to Structural Reallocation; How Inflation Has Reshaped Everyday Life in Tanzania

Africa enters a more cautious consumer phase in March as sentiment dips close to zero

Trust Is Becoming Economic Infrastructure