Davies Nyachieng'a

December 22, 2020

Share article

December 21, 2020 1:14 PM

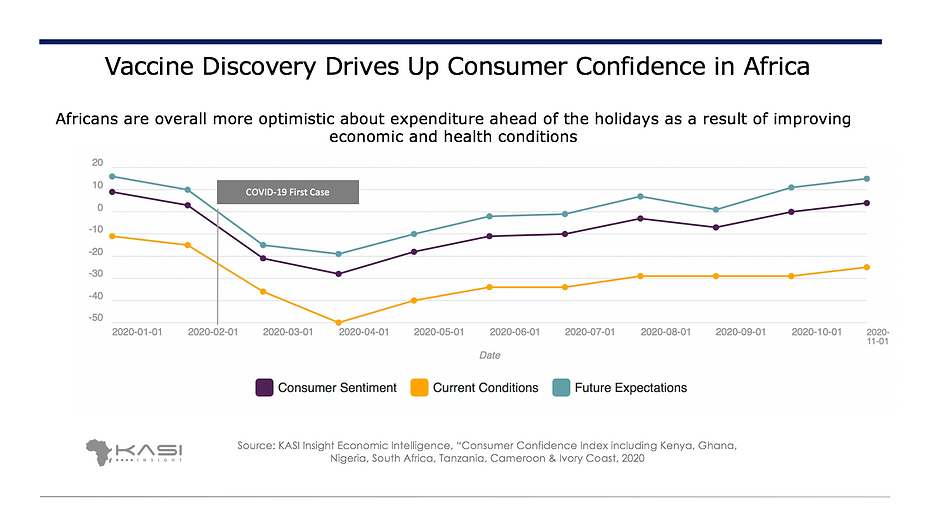

Africa’s consumer confidence crossed into positive territory this month rising to 4 from 0 supplementing the progress made in October. After stagnating last month, the index of current economic conditions finally moved up by 4 points climbing to -25 from -29. Meanwhile, the index of future expectations maintained its upward trend this month as it ascended by 4 points to 15 from 11.

In November, there was vast jubilation and relief across the world as effective COVID-19 vaccines were discovered by pharmaceutical companies notably from Pfizer (in collaboration with BioNTech), Moderna, and AstraZeneca (in collaboration with Oxford University). While the discovery of the vaccines has led to global optimism, there exist supply-chain challenges particularly in the distribution of the vaccine. For example, the Pfizer/BioNTech vaccine has to maintain a recommended storage temperature conditions of -70°C±10°C for up to 10 days unopened, thus posing challenges in transporting the vaccine. Nonetheless, some African countries like South Africa are making efforts in preparing to acquire the vaccine by participating in WHO’s Global Vaccine Access Facility.

Data from the Africa CDC shows that, as of 18th December 2020, the number of COVID-19 cases in Africa stood at 2,449,754 with 57,817 deaths and 2,073,214 recoveries.

With the holiday season here, the outlook for households is positive. This is manifested by the gains in the indices tracking households’ perception of the economic and financial conditions. Both indices tracking the general economic conditions in the city and country experienced a 4-point increase backed by the discovery of the COVID-19 vaccines as well as the continued reopening of economies. The prevailing low-inflation, low-interest-rate environment remained favorable to households’ financial situation. Discretionary spending and household income saw the largest growth as both their indices expanded by 6 points. Households’ purchasing power index also heightened by 3 points while the personal finance index was unchanged. Job prospects finally improved after two successive months of lackluster performance. The index gained 4 points after remaining flat in September and receding by 3 points in October. Despite this rebound, the job prospects index still languishes in negative territory at -50.

For the 2nd month in a row, Tanzania’s consumer confidence had the best performance. After several months of fluctuating, Tanzania’s consumer confidence index has finally maintained a trend. This is great for retailers in the country as it reduces the level of uncertainty they had been facing in recent months. The index gained 15 points climbing from 22 to 37. This increase can be attributed to advancement in the index of future expectations and the index of current economic conditions which grew by 15 and 11 points respectively. The official swearing-in of President Magufuli for a 2nd term and a decrease in the monthly inflation rate of 0.1% drove up optimism in the country. Tanzanian households felt that general economic conditions in the country and city were better as both indices rose by 26 points. Furthermore, job prospects, which declined last month, bounced back by 23 points while household income expanded by 26 points. In spite of these improvements in job prospects and household income, the purchasing power and discretionary spending indices flatlined in November whereas the personal finance index fell by 1 point.

Cameroon had the worst-performing consumer confidence index for November. Its index declined by 7 points from 2 to -5. Similarly, its index of future expectations followed the exact pattern decreasing from 2 to -5 while its index of current economic conditions fell from 2 to -4. An increasing incidence of separatist violence between English-speaking states and the French-majority country during the regional council elections held early in December negatively impacted the outlook among households. While there was growth in the country’s general economic conditions index of 4 points, all the other indices deteriorated with the exception of the job prospects index which stagnated. The indices tracking general economic conditions in the city and household income both slid by 3 points whereas the personal finance, purchasing power, and discretionary spending receded by 19, 13, and 12 points respectively.

The positive outlook among African consumers is good news for retailers even for those in the discretionary goods space as there has been an uptick in discretionary spending by consumers over the past 2 months. However, while the outlook appears to be better, a recent holiday survey by KASI shows that only 19% of the respondents are looking to spend more on gifts this holiday season compared to last season due to the economic uncertainty brought about by the pandemic. Nevertheless, December should be a good month for retailers relative to the recent months as 50% of the respondents to the holiday survey expect to finish the majority of their shopping in December or later. Moreover, according to the survey, it will be vital for retailers to invest in COVID-19 measures within their stores as the survey shows that 66% of respondents prefer shopping physically rather than online for holiday products.

“The discovery of a COVID-19 vaccine is certainly wonderful news for the world but there is still a great challenge in distributing and administering the vaccine to all parts of the world. As such, retailers must be cautious in hastily returning to their pre-Covid modes of operation as it could take several months before the majority of the population is eventually inoculated,” said Davies Nyachienga, Economic Intelligence Group at Kasi.

About the methodology

Kasi Consumer Confidence Score (Kasi CCI) is a composite index compiled from a seven-question survey that runs monthly via our consumer polls in the countries covered. The data output is based on a fresh, randomly selected representative sample of city dwellers aged 18-64. Released the first week of every month, Kasi CCI provides a focused view on consumer perceptions in seven African urban centers (Ghana, Nigeria, Kenya, South Africa, Cameroon, Ivory Coast, Tanzania) where most spending in the continent is concentrated.

For each question, the final metric will be a ‘balance measure’ of the percentage of positive responses minus the percentage of negative responses. The overall metric will be an average across all the questions.

Contact our team today to explore how our consumer intelligence can empower your decision-making process. Win with confidence with Kasi insights https://www.kasiinsight.com/request-demo/

1265 views

Share article

Financial pressure in Ghana is shaping emotional wellbeing differently across income and age groups

The Hidden Cost of “Managing”: Egypt’s Middle Class is Trading Health for Financial Survival

Mpox outbreak in Africa exposes critical inequities in global health