Paul Cheloti Mulongo

December 18, 2024

Share article

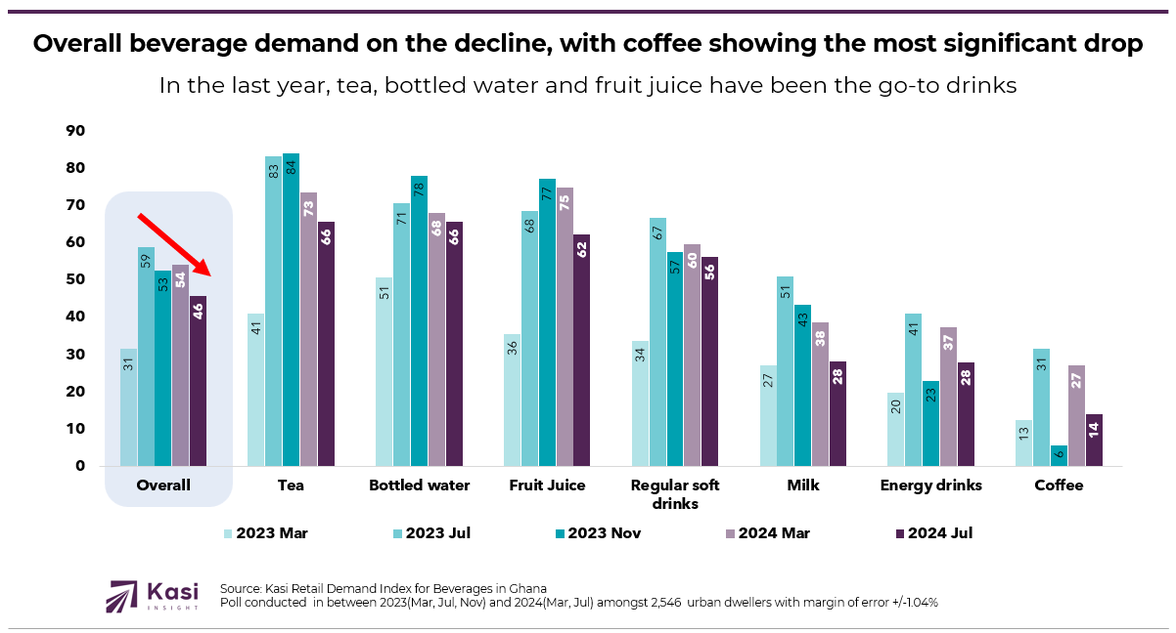

The Kasi Retail Demand Index provides valuable insights into consumer demand for various retail categories in Ghana. Ranging from +100 to -100, the index measures how consumer habits influence demand across different categories. A higher index value indicates strong consumer interest and purchasing intent, while a lower value suggests decreased demand. Looking at 2023 to 2024 data, the retail demand index for beverages in Ghana reveals an overall decline. While overall demand peaked in July 2023, the market has since experienced fluctuations, with bottled water and tea consistently leading demand, even as coffee continues to struggle. Between March 2023 and July 2024, tea emerged as a favorite, consistently holding a high demand index, peaking at 84 in November 2023 before settling at 66 in July 2024. Similarly, bottled water has shown steady popularity, with demand reaching an all-time high of 78 in November 2023 and slightly declining to 66 by July 2024.

Fruit juice has also performed well, with a robust index of 77 in November 2023 and a steady position in 2024 despite a mild drop to 62 in July. In contrast, categories like milk, energy drinks and coffee exhibit more volatility and have struggled to capture consumer interest. Coffee’s demand remained particularly low, hitting a mere 6 in November 2023 and recovering slightly to 14 in July 2024.

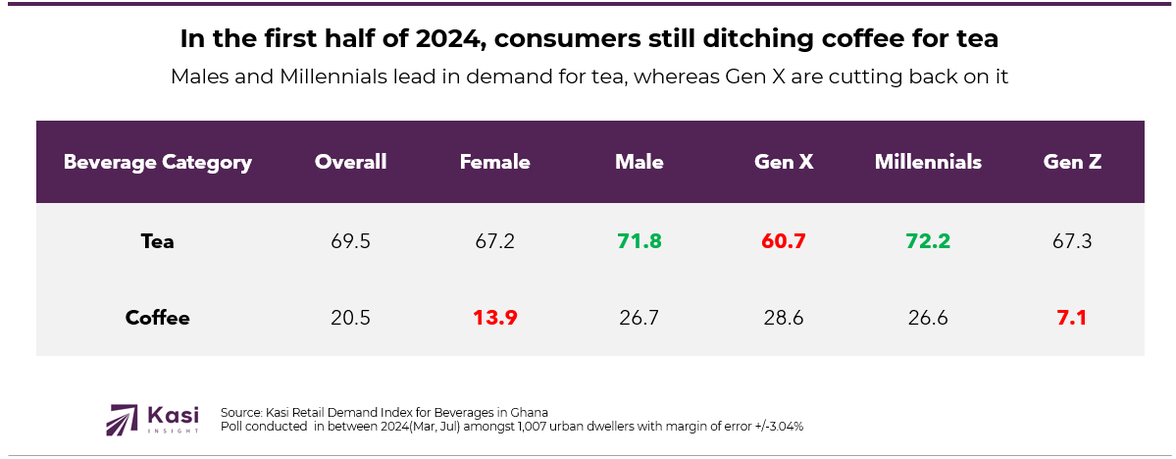

When analysing demand trends for tea and coffee in the first half of 2024, tea has continued to lead the market with a retail demand index of 69.5, far surpassing coffee, which shows an index of 20.5, the lowest of all beverages tracked. Tea is particularly popular among Millennials, who lead the charge with an index of 72.2, followed closely by Gen Z at 67.3. Gen X lags behind at 60.7, although they still prefer tea over coffee.

Conversely, coffee struggles to find a strong consumer base. Men show a higher preference for coffee (26.7) than women (13.9), but both genders rank it far behind tea. Interestingly, Gen X is the leading demographic for coffee, with an index of 28.6, while Millennials follow at 26.6. Gen Z shows minimal interest in coffee, with a notably low index of 7.1, reflecting their limited engagement with this category.

The Ghanaian beverage market presents both challenges and opportunities for brands. With bottled water and tea leading demand, these categories represent key areas for growth and market expansion. Brands can leverage this sustained demand by introducing innovative flavor profiles, eco-friendly packaging, and health-focused marketing campaigns.

Meanwhile, the low demand for coffee and energy drinks highlights a gap that brands can address through targeted strategies. For example, positioning coffee as a lifestyle beverage for busy professionals could resonate with Gen X and Millennials, while highlighting the health and energy benefits of energy drinks might appeal to younger consumers.

Brands should also tailor their campaigns based on demographic insights. Millennials are the key consumers driving tea demand, making them an ideal target for premium or organic tea products. Gen Z, with their relatively high demand for tea and low interest in coffee, could respond well to campaigns emphasizing affordability and wellness.

Share on socials using this caption: Ghana’s beverage market is evolving! 🍵💧 Tea and bottled water are leading demand, while coffee lags behind. Discover the trends shaping consumer behavior in 2025! #ConsumerTrends #Ghana #BeverageDemand #TeaVsCoffee #Millennials #GenZ

2263 views

Share article

Cameroon’s protein market in 2026 is shifting from habitual consumption to structured and intentional demand

Consumer Choices Post COVID-19 Are Redefining Kenya’s Beverage Landscape

Nigeria’s alcoholic beverages market shows resilience in beer but steep H1 declines in premium categories