Sandra Beldine Otieno, MSc

September 8, 2025

Share article

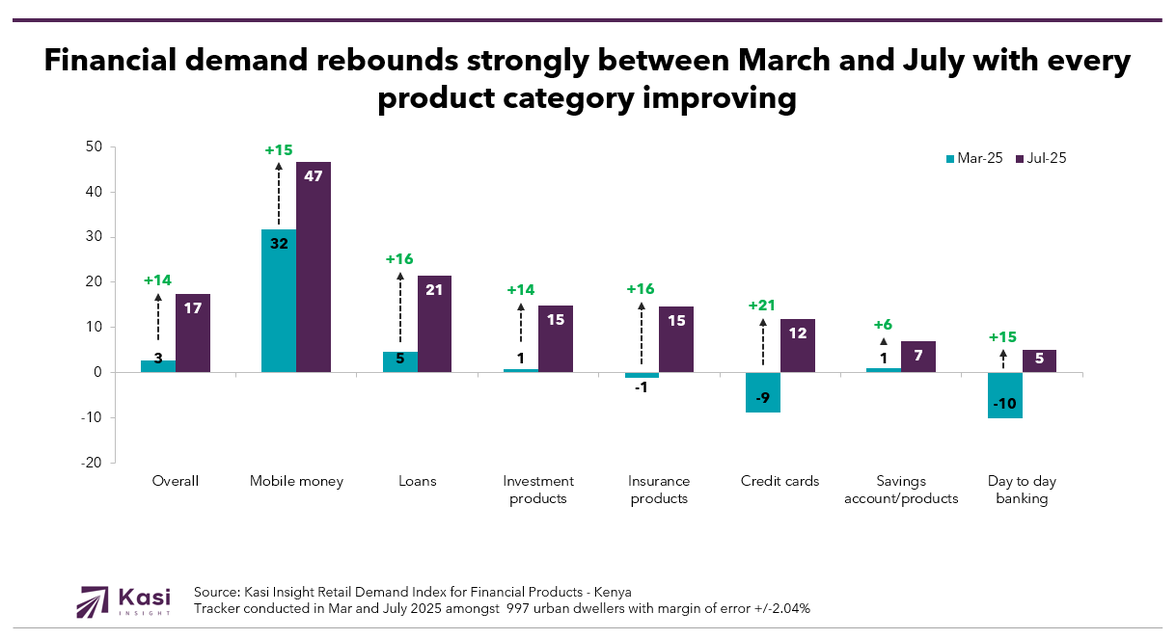

Kasi Insight’s Retail Demand Index (RDI), tracked quarterly, provides a forward-looking view of how consumer demand is evolving across consumer-facing categories. With a scale from +100 to -100, the index reflects shifts in consumer interest and purchasing intent. In Kenya, the comparison between March and July shows a decisive rebound in financial services demand, with the overall index climbing by 14 points. This swing signals renewed optimism and almost immediate changes in how Kenyans are borrowing, saving, and investing.

The rebound in July is best explained against the backdrop of Kenya’s aggressive monetary easing. The Central Bank of Kenya cut the policy rate five times in succession, from 10.75% in February to 10.00% in April, 9.75% in June, 9.50% in July and finally 9.25% in August. This was the fastest sequence of reductions in more than a decade, aimed at lowering borrowing costs, easing liquidity pressures and stimulating both consumption and investment. The RDI shows how quickly these policy shifts translated into consumer behavior.

Loans were the first to respond, with demand rising from an index score of 5 in March to 21 in July as households and businesses moved to take advantage of cheaper credit. Insurance, which had been subdued, rebounded from -1 to 15, a sign that consumers were once again willing to pay for financial protection as conditions stabilized. Credit cards recorded the most dramatic shift, moving from -9 in March to 12 in July, underscoring renewed confidence in discretionary spending and short-term borrowing.

Investment products also benefited from the friendlier environment, climbing from 1 to 15 as high-income households diversified their portfolios. Day-to-day banking, which had been negative at -10, recovered to 5, while savings improved modestly from 1 to 7. Mobile money, already the strongest category, extended its dominance by rising from 32 to 47. Taken together, these movements suggest that consumers reacted almost immediately to the central bank’s decisions. Lower interest rates created breathing space for households, encouraging them to borrow with greater confidence, re-engage with insurance and cautiously step back into investment products.

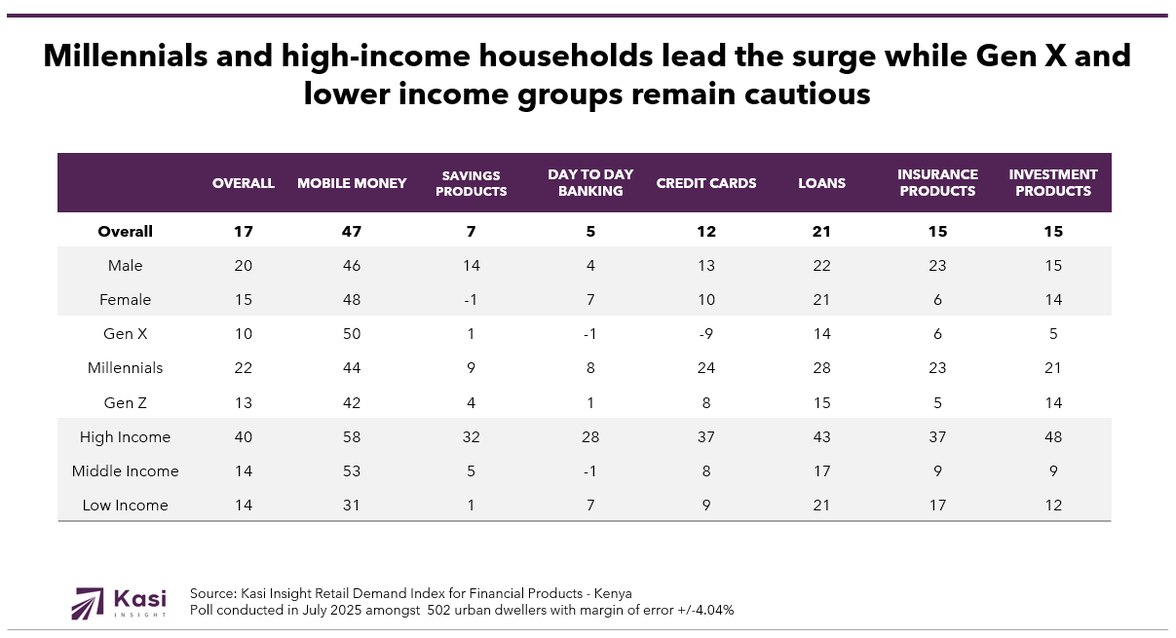

The July breakdown of the index highlights the demographic forces behind this resurgence. Millennials recorded the highest demand across nearly every category, with scores of 28 for loans, 24 for credit cards, 23 for insurance and 21 for investments. Their willingness to borrow and diversify into financial products positions them as the generation setting the pace of recovery. Gen Z follows a similar trajectory, though with more cautious scores, while Gen X remains restrained, particularly in credit cards and day-to-day banking, where demand remains negative.

Income segmentation reveals an even sharper divide. High-income households are fueling the surge, posting demand scores of 43 for loans and 48 for investments, evidence of confidence in leveraging cheaper credit while expanding into wealth-building products. Middle-income and low-income groups recorded more modest gains, with growth centered on mobile money, which scored 53 and 31 respectively. Gender dynamics add another layer of complexity. Men are driving demand for savings and insurance, while women remain the backbone of mobile money adoption, scoring 48 compared to 46 for men.

The RDI confirms that Kenya’s financial recovery is real but uneven. For banks, the surge in loans and credit cards among millennials is an opportunity to introduce structured, transparent credit products that build trust and strengthen long-term relationships. The rising appetite for investments and insurance among high-income households signals demand for wealth management solutions that are both digital and personalized. The rebound in day-to-day banking shows that traditional institutions still matter, but their relevance will depend on convenience, trust and integration with digital channels.

For fintechs, the opportunity lies in building on the ubiquity of mobile money. Women and lower-income households already rely on it daily, but the next wave of growth will come from embedding micro-savings, micro-insurance and entry-level investment tools directly within the platform. By expanding its functionality, fintechs can transform mobile money from a transactional tool into a pathway for long-term financial inclusion.

Kenya’s financial sector is entering a new cycle of growth. The signals from the RDI are unambiguous: demand is rising across credit, insurance and investments, millennials are leading the charge, high-income households are accelerating, and mobile money remains indispensable. The winners in this next phase will be the providers who recognize these divergences and adapt their strategies quickly to match the new shape of consumer demand.

Share on socials using this caption: 📊 Kenya’s financial appetite is back on the rise! Between March and July, Kasi Insight’s RDI shows strong growth in loans, insurance, investments, and mobile money 💳📈 Millennials and high-income earners are driving the rebound, while mobile money continues to anchor inclusion 🌍💡 #KenyaFinance #RDI #Fintech #Banking #ConsumerTrends

2732 views

Share article

How Consumer Sentiment Predicts Kenya’s Credit Cycles

Generational housing gap widens as younger Kenyans face rising barriers to home ownership

Financial services in Ivory Coast earn trust for delivery but fall short on transparency