Sandra Beldine Otieno, MSc

September 10, 2025

Share article

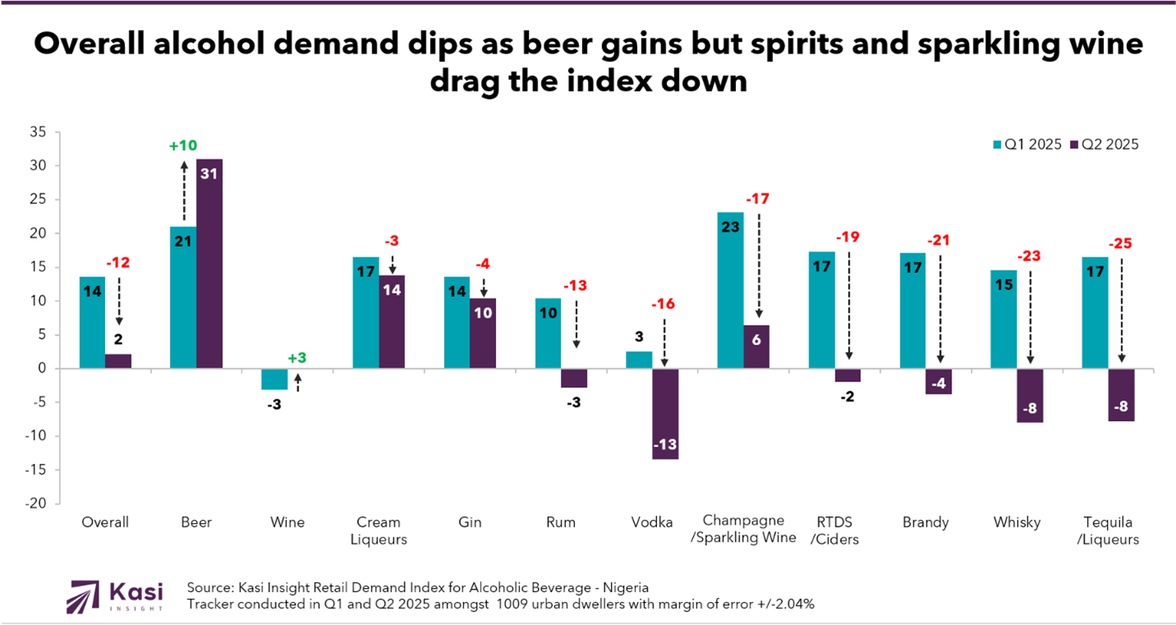

Kasi Insight’s Retail Demand Index, measured quarterly, provides a clear picture of how consumer demand evolves across categories. With a scale from +100 to -100, the index reflects consumer interest and purchasing behavior. In Nigeria, the first half of 2025 revealed a sharp slowdown in alcoholic beverages, with the overall index falling from 14 in the first quarter to 2 in the second. This shift signals that consumers are pulling back, yet the details reveal a polarized market where staples gain traction while premium categories collapse.

The second quarter highlighted a widening gap between resilient everyday drinks and aspirational categories. Beer was the strongest performer, rising 10 points to 31 and cementing its status as the most accessible and widely consumed beverage. Wine, though traditionally weaker in demand, inched up 3 points to reach neutral territory at 0, suggesting a tentative re-entry into consumer baskets. Cream liqueurs and gin softened slightly but remained in positive territory at 14 and 10.

The decline of premium and lifestyle drinks was far more dramatic. Champagne and sparkling wine fell by 17 points to 6, a sharp reversal for a product often linked to celebration and status. Ready-to-drink ciders and fruit-flavoured alcohol, typically associated with youth culture, dropped by 19 points into negative territory, showing that even younger consumers are cutting back. Whisky and tequila recorded the steepest declines, falling 23 and 25 points respectively, both ending well below zero. The data reveals a clear reset in consumer priorities. Aspirational categories that once signaled success or celebration are increasingly sidelined as households choose value-driven beverages instead.

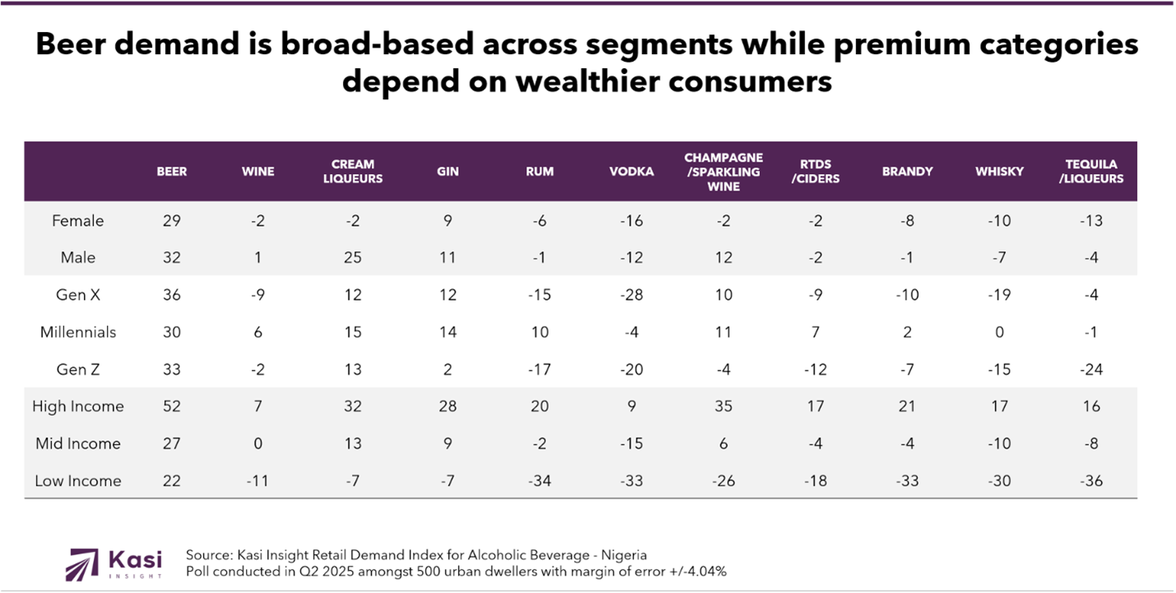

The second quarter also revealed a market increasingly defined by consumer segmentation rather than category performance alone. Male consumers posted stronger demand across most beverages, including beer at 32 and cream liqueurs at 25, while female scores were consistently weaker, particularly in premium categories such as champagne and tequila. This indicates that men are currently driving both mass and premium demand, while female participation is narrowing to more selective categories.

Generational and income contrasts amplify this divide. Millennials emerged as the most versatile drinkers, balancing practicality and aspiration with strong demand for beer at 30, gin at 14, and champagne at 11. Gen Z, in contrast, leaned heavily toward affordability, sustaining beer at 33 but retreating sharply from spirits like whisky and tequila where demand collapsed into negative territory. Income levels further split the market. Affluent households sustained premium indulgence, driving champagne to 35, cream liqueurs to 32, and whisky to 17. By contrast, low-income groups have almost entirely withdrawn from the alcohol market, recording deep negatives across rum, brandy, and vodka. These patterns underscore how consumer priorities are increasingly shaped by affordability and lifestyle choices rather than by overall category performance.

Alcoholic beverage brands face their most decisive moment of the year as the festive season drives peak consumption. Beer will remain the dominant choice across genders, generations, and income groups. Multi-pack promotions, family-sized bundles, and community activations can unlock scale, while campaigns tied to football, music, and social gatherings will strengthen beer’s role as the drink of choice for shared celebrations. Premium categories still hold promise among affluent households that view the season as a time for indulgence and gifting. Champagne, whisky, and liqueurs can thrive if positioned as symbols of prestige, supported by exclusive packaging, curated assortments, and luxury experiences.

The middle-income segment represents the swing group. Although cautious, these consumers can be re-engaged through affordable premium substitutes, promotions that emphasize value, and experiential activations linked to nightlife and cultural festivals. Across all segments, responsible and culturally grounded marketing will be essential. Campaigns that emphasize family, togetherness, and moderation will resonate strongly in a season defined by community and tradition. The brands that succeed will be those that balance affordability with aspiration, securing immediate festive gains while building loyalty that extends into 2026.

Share on socials using this caption: 🍺 Nigeria’s drink scene is shifting fast! Beer is booming while premium spirits lose their sparkle ✨. With households tightening budgets, value now beats aspiration, but the festive season still holds space for indulgence among the affluent. Brands that balance affordability with prestige will win both 🎉🥂. #Nigeria #ConsumerTrends #Beer #Whisky #Champagne #KasiInsight #HolidaySeason #MarketInsights #BeverageIndustry

1956 views

Share article

Fresh staples stay strong as Nigeria’s food market splits between value seekers and quality spenders

Ugandans are loyal to beer but wine captures the biggest spend

Tanzanian consumers are balancing value and purpose in their food purchases