Catherine Wangari

January 26, 2024

Share article

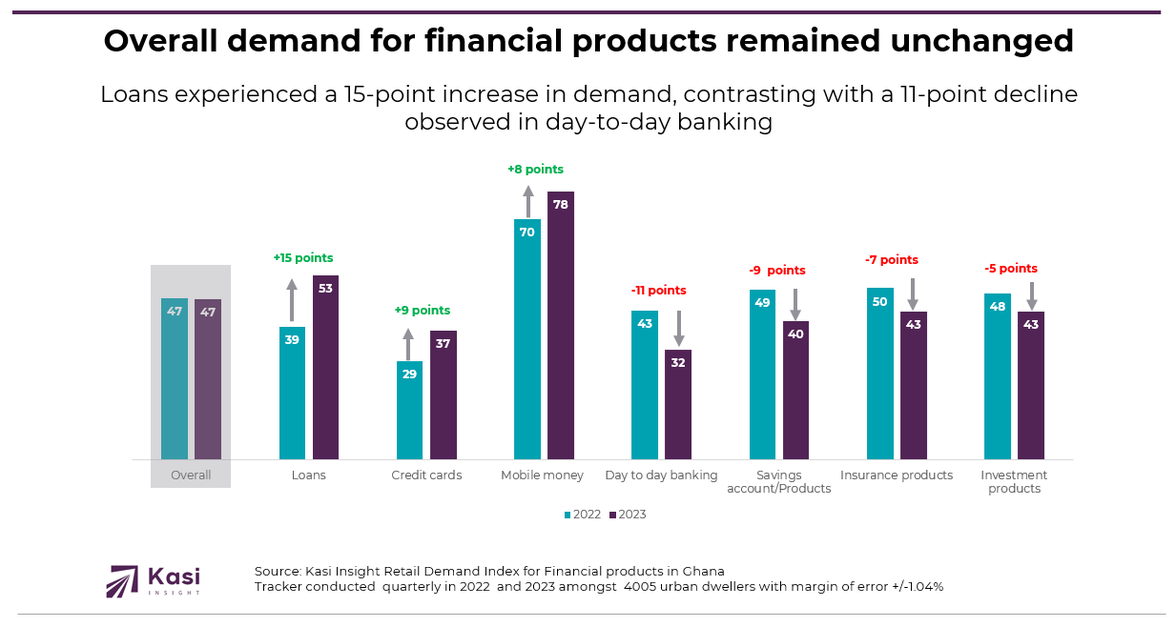

The Kasi Retail Demand Index monitors consumer demand for retail categories in 21 African markets, providing quarterly insights into how consumer habits impact category demand. Measured on a scale from +100 to -100, a level close to 100 indicates high demand, with more consumers seeking purchases, while a level near -100 signals low demand. In Ghana, the index revealed that demand for financial products remained consistent from 2022 to 2023.

While the overall demand for financial products remained relatively steady, specific categories within the financial sector witnessed notable shifts. There was a considerable surge in the demand for loans, experiencing a significant uptick of 15 points. This suggests an increased inclination towards borrowing within the consumer base. Credit cards and mobile money also saw positive trends, with demand rising by 9 and 8 points, respectively, indicating a growing preference for convenient and flexible financial tools.

Conversely, day-to-day banking experienced an 11-point decline, signalling a potential shift in how consumers approach routine financial transactions. The drop in demand for savings accounts by nine points implies a reassessment of traditional savings practices. Furthermore, there were declines of 7 and 5 points for insurance and investment products, respectively.

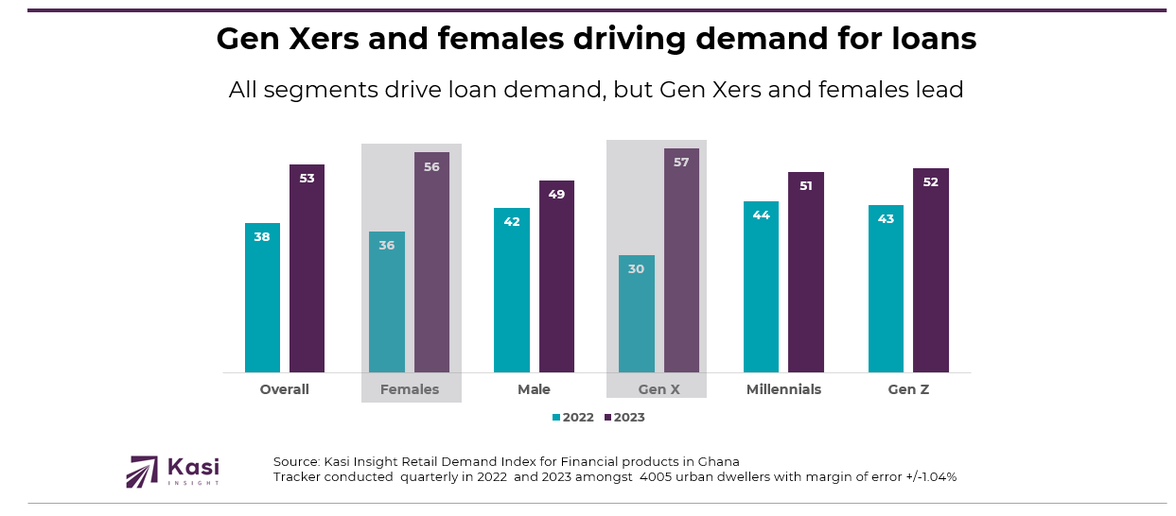

Analyzing loan demand from 2022 to 2023 highlights significant shifts across demographic segments. The overall demand reflects a substantial 15-point increase, indicating a notable surge in the desire for loans. The Gen X cohort stands out with an impressive 27-point surge, showcasing a significant transformation in borrowing behaviour within this age group. For females, there's a substantial evolution, with demand rising by 20 points from 36 to 56. Males experience a more measured increase of 7 points, moving from 42 to 49.

Millennials see a moderate 8-point uptick, from 44 to 51, while Gen Z displays a robust 9-point increase, moving from 43 to 52. These nuanced changes underscore a dynamic landscape of evolving loan demand preferences within specific demographic categories, reflecting varied borrowing behaviours across different age groups.

For financial brands in Ghana, the evolving landscape of loan demand signifies crucial insights and opportunities. The substantial 15-point increase in overall demand indicates a heightened inclination towards borrowing within the consumer base. This signals an opportune time for financial institutions to tailor their offerings, potentially introducing innovative loan products or refining existing ones to meet the growing demand.

The positive trends observed in credit cards and mobile money, with demand rising by 9 and 8 points, respectively, highlight a growing preference for convenient and flexible financial tools. Brands can leverage this shift by enhancing and promoting their credit card and mobile money services, ensuring they align with the evolving preferences of the Ghanaian consumer.

However, the 11-point decline in day-to-day banking suggests a potential shift in how consumers approach routine financial transactions. Financial brands should reassess their digital banking offerings and user experience to ensure they meet the changing expectations of their customers. The drop in demand for savings accounts by nine points implies a reassessment of traditional savings practices. Brands may need to reevaluate and enhance their savings account offerings, possibly introducing features that align with modern financial goals and preferences.

Share on socials using this caption: Unlocking the financial dynamics of Ghana 🌍💰 Dive into the trends from 2022 to 2023: a surge in loans, shifting preferences, and insights into Gen Xers and females leading the financial charge! 📊💡 #FinancialShifts #GhanaFinance #DemographicInsights

2340 views

Share article

Equity leads where financial journeys begin, while the greatest opportunity lies in capturing more value as those journeys mature.

The Rise of Behavioral Intelligence in African Investing

The Signal Investors Are Missing in African Equity Markets