Alison Okatch

June 5, 2026

Share article

The Kasi Cost of Living Survey tracks how Tanzania consumers have experienced and responded to rising prices between 2022 and 2026. Conducted across multiple waves, the study captures evolving perceptions of affordability, financial wellbeing, and household coping strategies, while providing insights into how these experiences differ across generations and gender groups.

After recovering steadily from the cost-of-living pressures that followed the COVID-19 period and the global commodity shock of 2022, Tanzanian consumers experienced improving financial conditions through much of 2024 and 2025. However, this recovery reversed sharply in early 2026, coinciding with the escalation of the Iran conflict that began on February 2026. The conflict heightened global economic uncertainty and renewed concerns around energy prices, trade flows, and inflation, contributing to a broad deterioration in consumer perceptions of financial wellbeing.

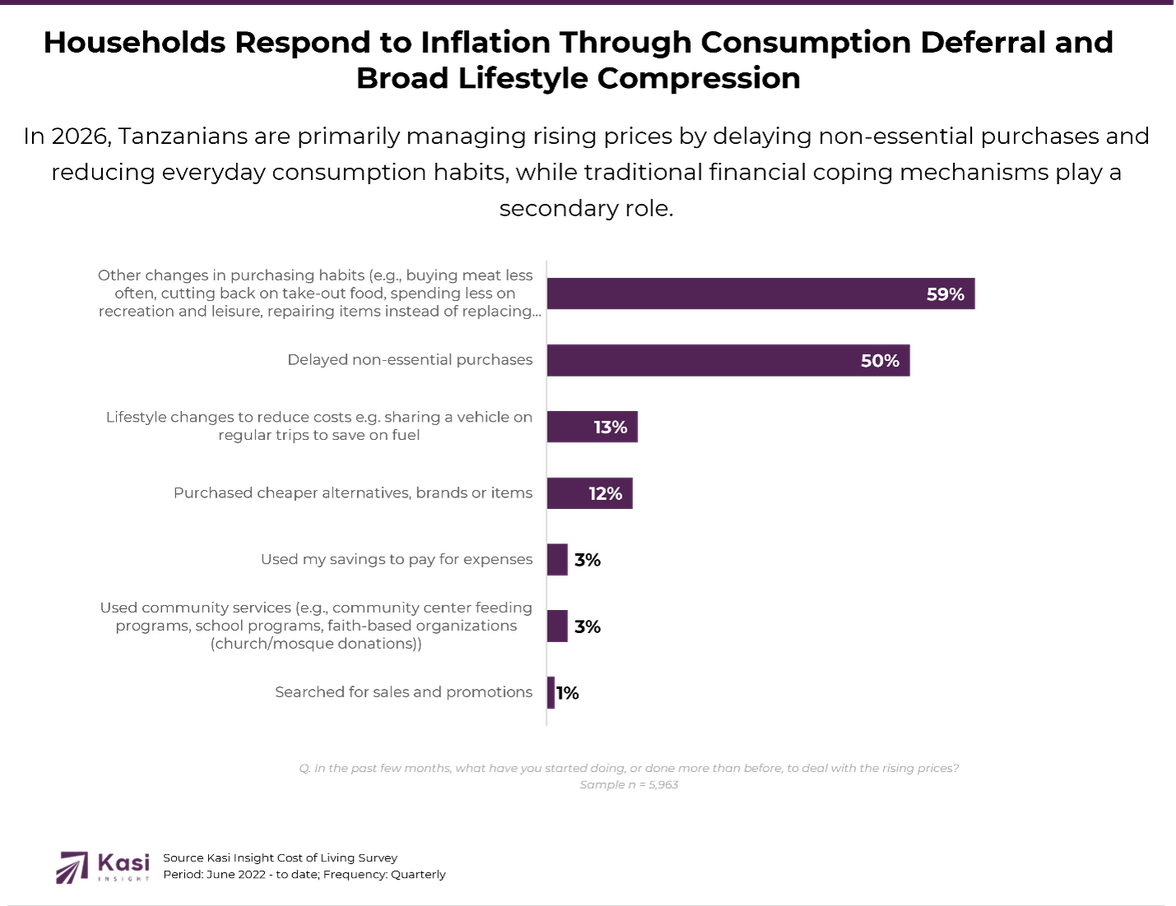

In response to this renewed pressure, households did not revert to earlier crisis-era coping mechanisms such as relying heavily on savings or shifting aggressively to cheaper substitutes. Instead, adjustment patterns in 2026 show a more structural shift in behavior, with consumers increasingly managing rising prices by reducing and postponing consumption rather than attempting to financially absorb or offset costs. This reflects a more entrenched form of adaptation, where inflation is managed through changes in what households choose to buy, and when they choose to buy it, rather than through short-term financial buffering strategies.

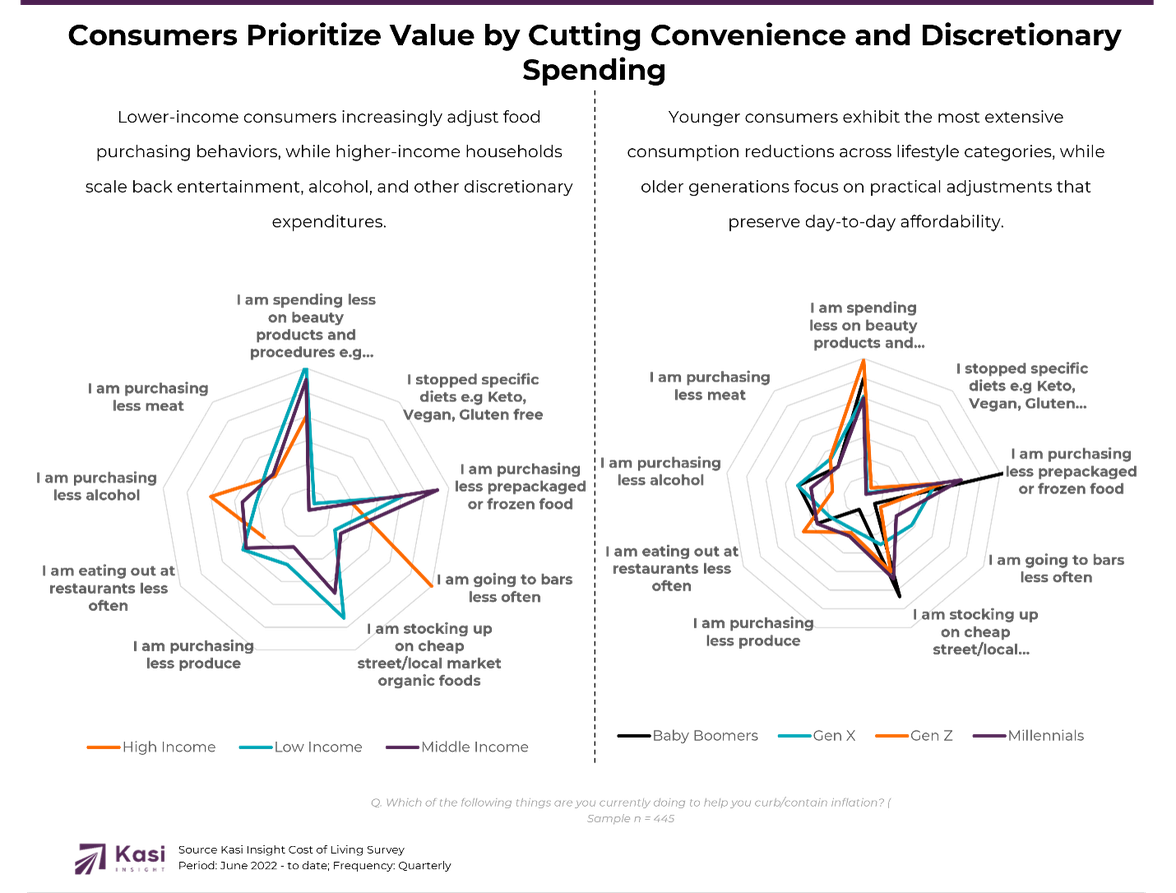

While the broader population has responded to rising prices by delaying purchases and reducing overall consumption, the categories affected vary significantly across consumer groups. This suggests that inflation is no longer producing a universal response; instead, households are making targeted trade-offs based on their financial flexibility, spending priorities, and stage of life.

Among lower-income households, coping strategies are concentrated around essential consumption. They are more likely to reduce produce purchases (11%), cut back on restaurant visits (15%), and increasingly rely on cheaper street and local market food options (23%). These behaviors indicate a strong focus on preserving affordability within everyday food spending.

Middle-income consumers exhibit a different adjustment pattern, showing the highest reductions in prepackaged and frozen foods (28%) while also increasing reliance on lower-cost food sources (18%). This suggests a shift away from convenience-driven purchases toward more value-oriented consumption.

High-income households, by contrast, remain relatively insulated from pressures on essential food categories but continue to scale back discretionary lifestyle spending. They are significantly more likely to reduce bar visits (30%), alcohol purchases (20%), and spending on beauty products and procedures (20%), indicating that inflation is primarily affecting non-essential consumption rather than basic needs.

Generational differences reinforce this pattern. Gen Z records some of the highest levels of reduction across multiple categories, particularly beauty spending (35%), restaurant visits (18%), and meat consumption (13%), reflecting a highly adaptive approach to affordability management. Gen X exhibits more balanced reductions across both essential and discretionary categories, consistent with greater household and family responsibilities. Meanwhile, Baby Boomers show a particularly strong shift away from prepackaged foods (40%) and toward lower-cost local food sources (27%), suggesting a preference for practical adjustments rather than broad lifestyle sacrifice.

Taken together, the findings indicate that inflation is not driving a uniform decline in consumption. Instead, households are selectively restructuring spending according to their financial circumstances and consumption priorities, resulting in distinct affordability management strategies across different segments of the population.

Inflation has evolved from a temporary affordability shock into a structural force reshaping consumer priorities, spending patterns, and category demand. As households become increasingly selective about where and how they spend, success will depend less on broad-based price reductions and more on delivering clear value within categories that consumers continue to prioritize.

For businesses, this means demand is becoming increasingly polarized. Lower- and middle-income consumers are actively trading down, seeking affordability and practical value, while higher-income households are concentrating cutbacks in discretionary lifestyle categories. Companies will therefore need to strengthen value propositions, expand affordable product formats, and align offerings with consumers' growing focus on necessity, utility, and spending efficiency.

For retailers and FMCG players, the shift toward local markets, reduced convenience spending, and increased scrutiny of non-essential purchases highlights the importance of value-pack architecture, affordable entry-price points, and products that demonstrate clear functional benefits. Premiumization opportunities will continue to exist but will require stronger justification and differentiation.

From a policy perspective, the findings suggest that while households have adapted to inflationary pressures, their resilience remains vulnerable to external shocks. The rapid deterioration in sentiment following renewed geopolitical tensions demonstrates that consumer confidence can reverse quickly, particularly when uncertainty affects food, energy, and transportation costs. Strengthening household resilience therefore requires not only inflation management but also broader efforts to improve economic security and protect purchasing power.

About Kasi Insight

Kasi Insight is Africa's leading decision intelligence firm specializing in high-frequency consumer and economic data across Africa. Through its proprietary survey infrastructure and analytics platform, Kasi provides real-time insights that help organizations anticipate economic shifts, understand consumer behavior, and make better strategic decisions.

We welcome collaboration with:

Organizations interested in exploring partnerships or accessing Kasi datasets are invited to contact our research team.

📧 yannick@kasiinsight.com

389 views

Share article

Africa's Consumer Confidence Slips Back Into Negative Territory in May

Assessment Of the Potential for Trade and Investment Exchanges Between Quebec and Africa

Africa enters a more cautious consumer phase in March as sentiment dips close to zero