Alison Okatch

April 30, 2026

Share article

The DRC media environment is no longer defined by which channels people can access, but by how credibility is constructed across them. What used to be a relatively linear funnel; TV driving awareness, followed by persuasion, is now a fragmented ecosystem where visibility, trust, and decision-making are distributed across competing sources of influence. The result is not media overload, but meaning overload: consumers are constantly triangulating what they see, hear, and experience before they believe anything.

This analysis draws on the Kasi Media Tracker, a monthly lens into how consumers access and process information across diverse media sources. It tracks evolving preferences in information channels, shifting patterns between digital and traditional media, and changes in both trust and engagement; providing a grounded view of how media behavior is reshaping decision-making in real time.

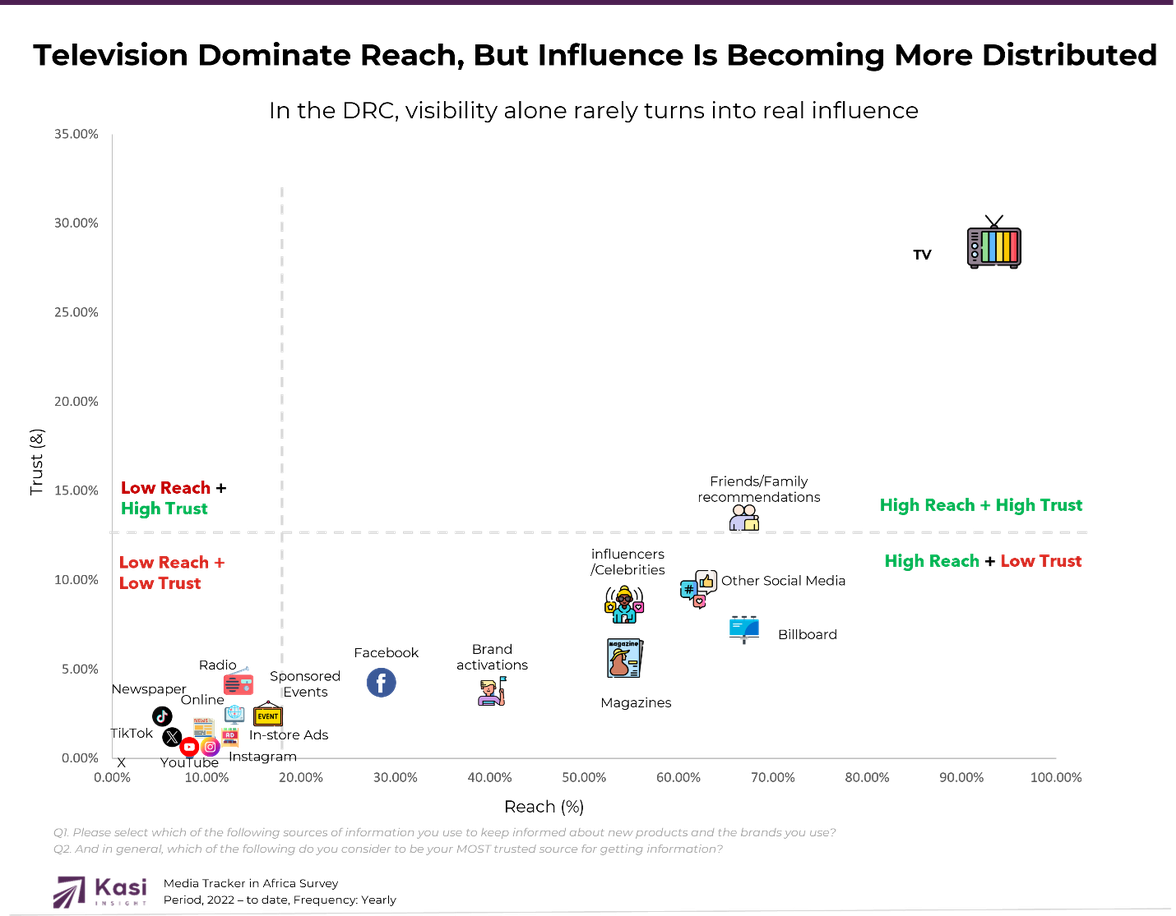

Television continues to dominate as the primary awareness channel in the DRC, with usage remaining consistently high at 94% in 2024, up from 91.6% in 2022. However, trust in television has softened over time, declining from 34% in 2022 to 29.1% in 2024.

This divergence between reach and trust is critical. Television is no longer the endpoint of persuasion; it is the starting point of validation. It still owns scale, but it no longer owns certainty. Consumers are exposed through TV, but decisions are increasingly confirmed elsewhere.

Friends and family recommendations have become increasingly influential, with usage rising sharply to 67.2% in 2024, while trust remains among the highest outside traditional media at 13.9%.

This reflects a deeper behavioral shift: trust in the DRC is becoming relational rather than institutional. Information is no longer evaluated on authority alone, but on proximity; who is saying it, and how close they are to lived experience. Even more importantly, trust is being “re-verified” socially after initial exposure elsewhere.

At the same time, exposure to influencers has grown significantly, reaching 54.1%, signaling the formalization of informal networks into structured persuasion systems. Influence is no longer accidental; it is increasingly engineered through personality-led credibility.

Physical channels are also gaining importance. Billboard exposure has grown substantially, reaching 66.5%, while brand activations and spokesperson-led communication have also increased meaningfully.

This points to a distinct market truth: in the absence of full media trust, repetition becomes a substitute for reassurance. High-frequency physical visibility is functioning less as advertising and more as validation; signaling that a brand is established, present, and economically real.

In the DRC context, “seen often” is increasingly interpreted as “safe to trust.”

While digital channels are expanding rapidly, trust remains anchored in traditional media. In 2024, 62% of consumers still identified traditional channels as their most trusted source, compared to 38% for digital.

This creates a structural tension: digital is becoming the discovery layer, but not yet the belief layer. Consumers increasingly encounter information online but still require offline reinforcement; through TV, physical presence, or interpersonal validation—to convert exposure into conviction.

The result is a hybrid trust system where no single channel completes the journey alone.

Most consumers spend limited time on social media, with the majority engaging for less than three hours per day. Streaming engagement is more stable, typically concentrated between one and three hours daily, positioning entertainment platforms as the most consistent digital attention environments.

This fragmentation matters less in terms of “screen time” and more in terms of “attention continuity.” Consumers are not deeply embedded in any single channel; instead, they move across multiple micro-moments of exposure, making repetition across platforms more important than intensity within any one platform.

The DRC media landscape is shifting from channel dominance to influence layering. Television still delivers unmatched scale, but it no longer controls interpretation. Trust is now built through reinforcement loops, where mass exposure is validated through social proof, physical visibility, and repeated encounters across fragmented environments.

For brands, the implication is clear: effectiveness is no longer about choosing the strongest channel, but orchestrating the most consistent presence. In this environment, credibility is not created by reach alone, but by alignment, where what is seen, what is said, and what is experienced all reinforce the same narrative until belief becomes inevitable.

Kasi Insight is Africa's leading decision intelligence firm specializing in high-frequency consumer and economic data across Africa. Through its proprietary survey infrastructure and analytics platform, Kasi provides real-time insights that help organizations anticipate economic shifts, understand consumer behavior, and make better strategic decisions.

We welcome collaboration with:

Organizations interested in exploring partnerships or accessing Kasi datasets are invited to contact our research team.

📧 yannick@kasiinsight.com

277 views

Share article

One Summit, Three Narratives, One Fight for Africa

Nigeria’s media preferences shift toward digital trust and audience-specific engagement

Ivorians blend digital and traditional media for accurate, trusted information