Sandra Beldine Otieno, MSc

January 27, 2025

Share article

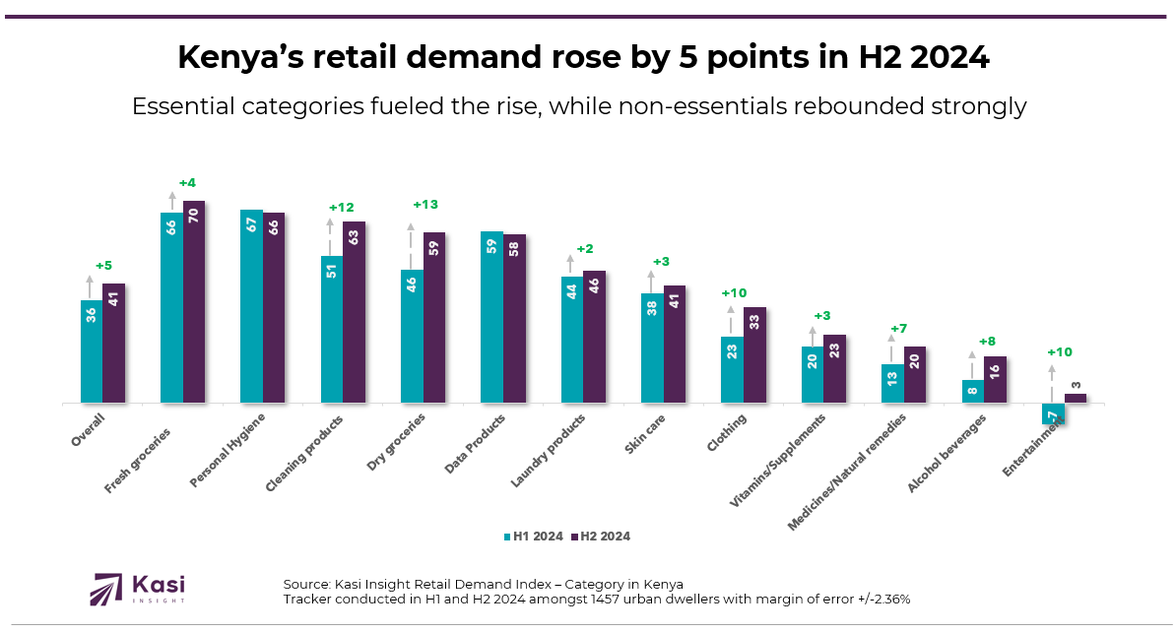

Kasi Insight’s Retail Demand Index (RDI), measured quarterly across 20 African markets, offers critical insights into how consumer demand is evolving across retail categories. Using a scale from +100 to -100, the index captures changes in consumer interest and purchasing behavior. In Kenya, a comparison between the first half (H1) and second half (H2) of 2024 revealed a dynamic shift in priorities, with the overall index rising from 36 to 41, highlighting increasing activity and diversification in the retail sector.

Household essentials drove much of this growth. Dry groceries recorded a significant 13-point surge, climbing from 46 to 59, while cleaning products followed closely with a 12-point increase to 63, reflecting heightened consumer focus on everyday necessities. Fresh groceries remained a core priority, rising by 4 points to a robust 70. Similarly, health-related categories such as vitamins/supplements and medicines/natural remedies posted steady gains, with increases of 4 and 6 points, respectively, signaling ongoing attention to personal wellness.

Discretionary categories also experienced a notable resurgence, reflecting shifts in consumer habits. Clothing demand rose by 10 points to 33, and entertainment saw a remarkable recovery, jumping 11 points from -7 to 3, indicating renewed interest in leisure activities. Alcoholic beverages experienced an 8-point increase, doubling demand from 8 to 16 as social preferences evolved. Meanwhile, personal hygiene and data products saw minor declines of 1 point each, likely reflecting stabilized demand or shifts in spending priorities.

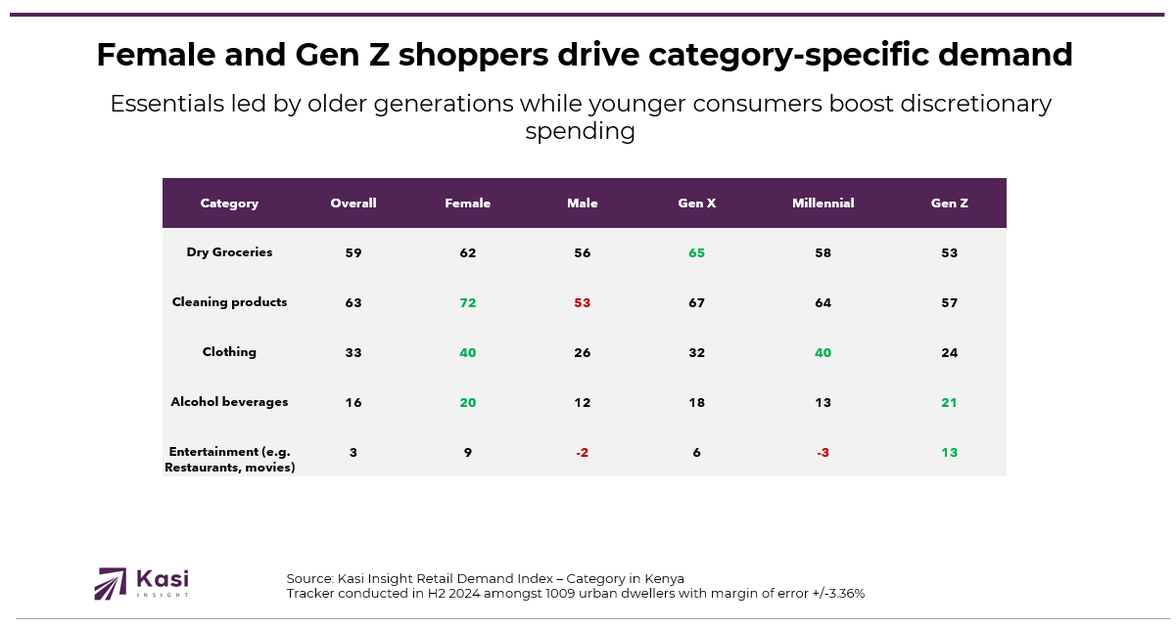

Retail demand in H2 2024 showcased diverse growth patterns, with distinct consumer segments driving performance across essential and lifestyle categories. Females took the lead in cleaning products, scoring an impressive 72 on the index, highlighting their strong focus on household hygiene and maintenance. Similarly, Gen X drove the demand for dry groceries with an index of 65, reflecting their prioritization of core household staples. Clothing saw a balanced contribution from females and millennials, both scoring 40, signaling shared interest in personal style and apparel among these demographics.

In discretionary categories, Gen Z stood out as a critical driver of demand. They led entertainment spending, with an index of 13, and showed the highest demand for alcoholic beverages at 21, emphasizing their preference for social and experiential consumption. While these categories saw growth, the patterns underline a generational split, with older demographics focusing on essentials and younger groups driving lifestyle and leisure spending.

Brands looking to succeed in Kenya’s retail market in 2025 must develop strategies that cater to the unique needs of different consumer segments. Essentials, such as dry groceries and cleaning products, remain vital categories driven by Gen X and female consumers, who prioritize practicality and household well-being. To resonate with these groups, brands should emphasize affordability and convenience, offering solutions like value packs, loyalty programs, or subscription-based models. Highlighting sustainability, such as eco-friendly packaging or sourcing, could also differentiate brands and build deeper loyalty with environmentally conscious shoppers. Health-related products like vitamins and natural remedies present opportunities for brands to strengthen trust by focusing on quality, transparency, and targeted wellness campaigns.

For discretionary categories, brands must recognize the growing influence of younger consumers, particularly Gen Z, who are driving demand for entertainment and alcoholic beverages. To capture their attention, brands need to prioritize digital-first strategies, including interactive social media campaigns and influencer partnerships, that reflect their social and experiential priorities. Offering immersive experiences, whether through events or collaborations, can create lasting impressions with this experience-driven demographic. Similarly, fashion and lifestyle brands targeting millennials and females should emphasize inclusivity, personalization, and sustainability to remain competitive.

Share on socials using this caption: 📈 Kenya’s retail sector is evolving! Essentials lead growth, but Gen Z is shaking up lifestyle trends in 2025. 🌱💃 Smart brands are adapting with sustainable, engaging strategies. Are you ready for the shift? 🚀 #KenyaRetail #ConsumerTrends #GenZ #Sustainability #MarketInsights #MarketingStrategy

2597 views

Share article

Uganda’s retail sector shows early 2025 fatigue as consumers cut back on essentials but remain engaged in wellness and lifestyle choices

Kenyan consumers are shifting from survival to intentional living reshaping value wellness and brand responsibility

Inflation fatigue is deepening financial stress for consumers in Ivory Coast