Alison Okatch

June 29, 2026

Share article

Financial freedom remains one of the strongest aspirations among African consumers, but the path to achieving it has become increasingly complex. While households continue to navigate the effects of rising living costs, economic uncertainty and persistent financial pressure, they have not abandoned their long-term ambitions. Instead, consumers are becoming more deliberate in how they define, pursue and measure financial success.

This analysis draws on Kasi Insight's Financial Services Tracker, covering consumer attitudes and behaviors across eight African countries over the past five years (2022–2026). The study explores how consumers define and pursue financial freedom, their financial behaviors and banking preferences, with results available by market, age group, gender and time to reveal evolving trends and opportunities for financial institutions.

For banks, this presents a strategic opportunity. As consumers seek partners that can help them build resilience rather than simply access financial products, trust will increasingly be earned through practical support, digital convenience and solutions that improve financial wellbeing.

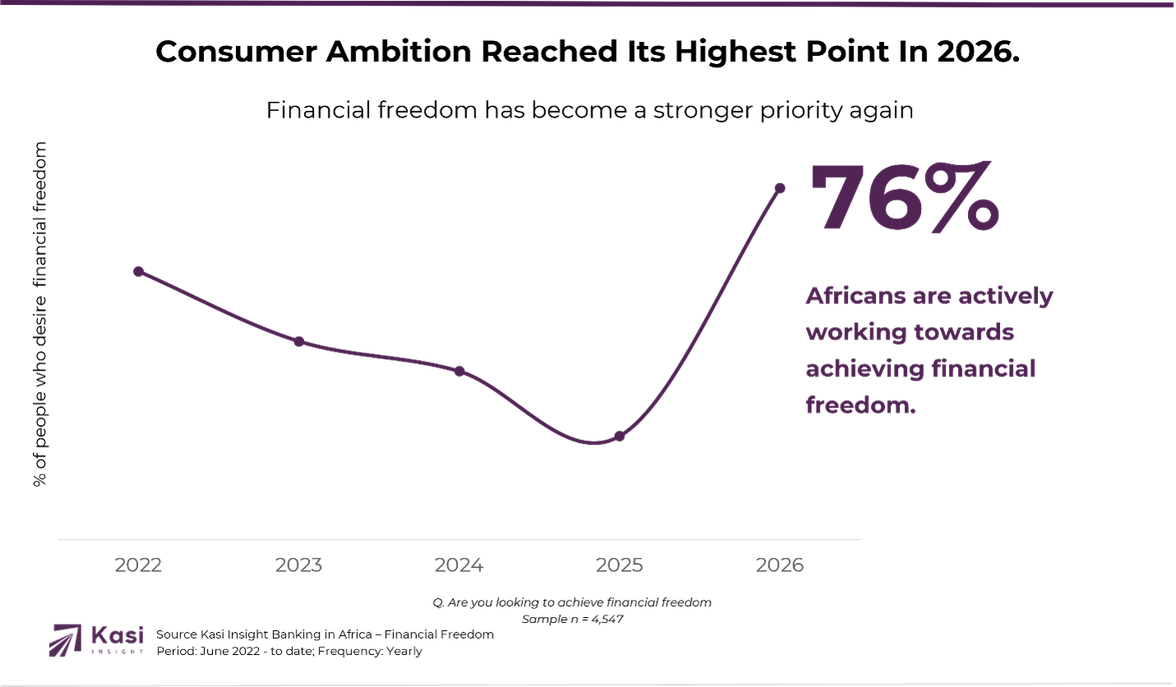

African consumers haven't given up on financial freedom; they're pursuing it more intentionally than ever.

Despite continued economic headwinds, financial ambition across Africa has strengthened. In 2026, 76% of consumers say they are working towards achieving financial freedom, rebounding from 61% in 2025 and marking the highest level recorded since 2022.

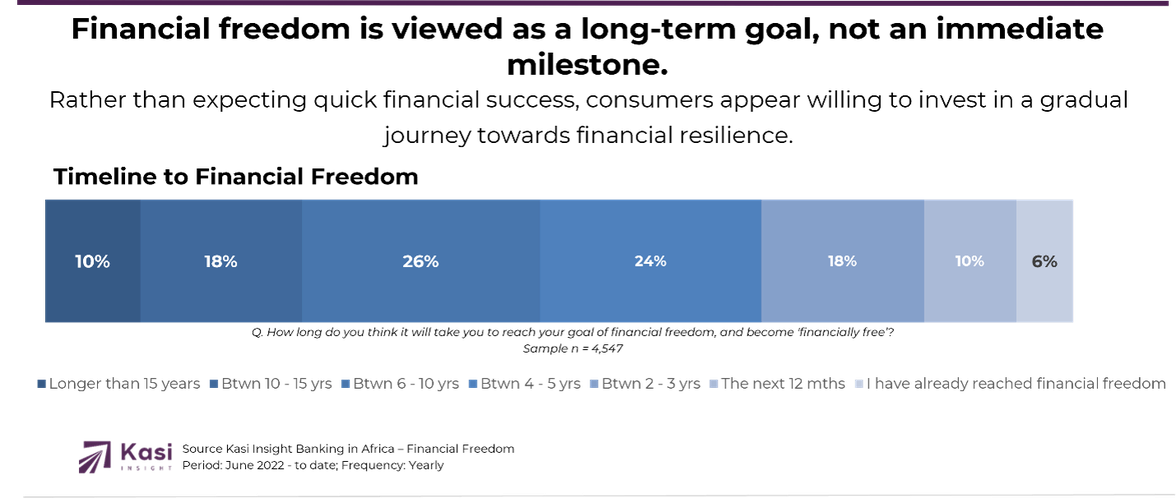

Economic pressure has not diminished ambition, it has sharpened it. Most consumers recognize that financial freedom is a long-term journey, expecting it to take between four and ten years, while a growing share believe it may take even longer. Only a small minority believe they have already achieved financial freedom or expect to do so within the next year.

Rather than chasing quick financial gains, consumers are adopting a more patient and disciplined outlook. Their optimism is grounded not in expectations of immediate prosperity, but in a determination to steadily improve their financial position over time.

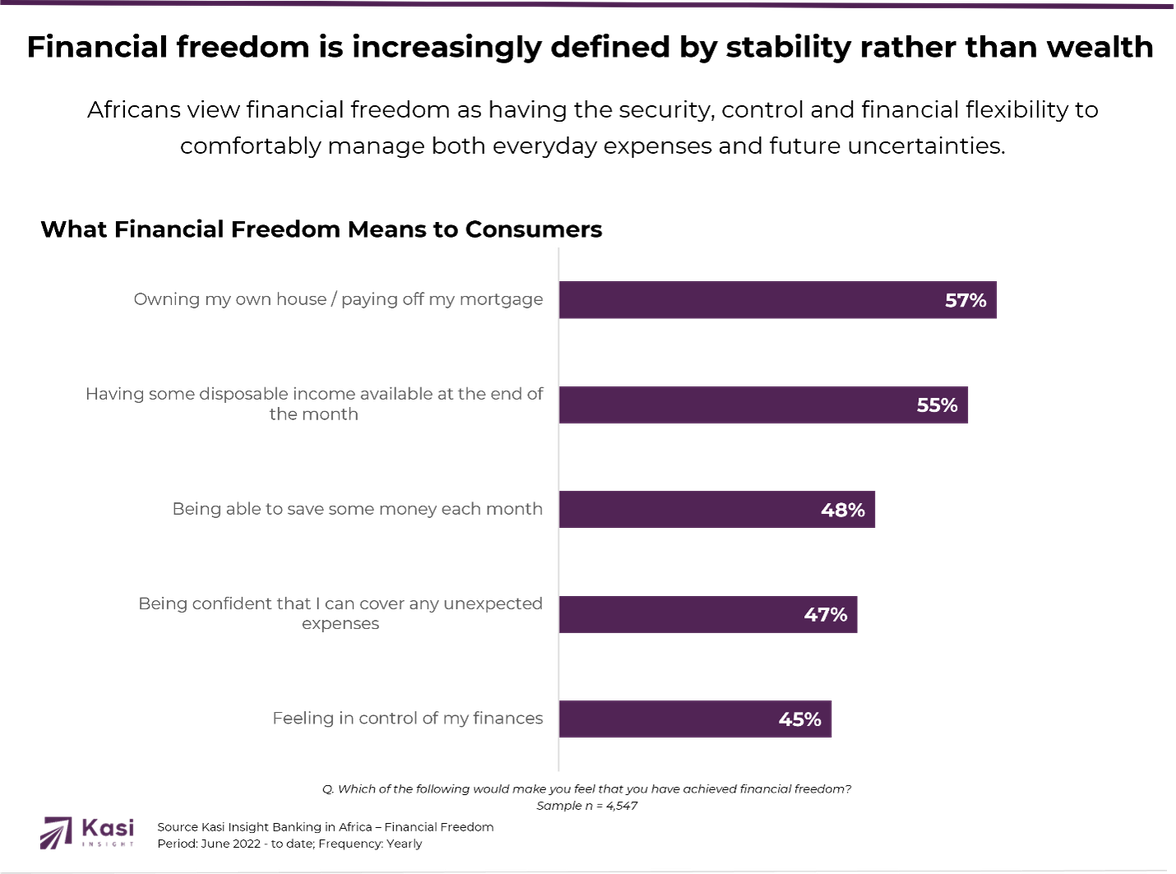

Financial freedom is no longer about being rich, it's about feeling financially secure.

Perhaps the most significant shift emerging from the data is how consumers now define financial freedom. Rather than focusing on wealth accumulation, they increasingly associate financial success with stability, control and resilience.

Consumers are most likely to define financial freedom as being on track to achieve important life goals such as buying a home or starting a business, having the flexibility to make lifestyle choices, feeling in control of day-to-day expenses and being able to absorb unexpected financial shocks. These priorities highlight the growing importance of financial preparedness in consumers' thinking.

When asked what would make them feel financially free, consumers prioritize practical milestones over luxury. Owning a home, having disposable income at the end of each month, saving consistently, paying bills comfortably and confidently covering unexpected expenses all rank ahead of traditional indicators of wealth.

Together, these findings point to a fundamental shift in priorities. Financial freedom is increasingly defined not by how much money consumers have, but by the financial certainty, stability and control they experience in everyday life.

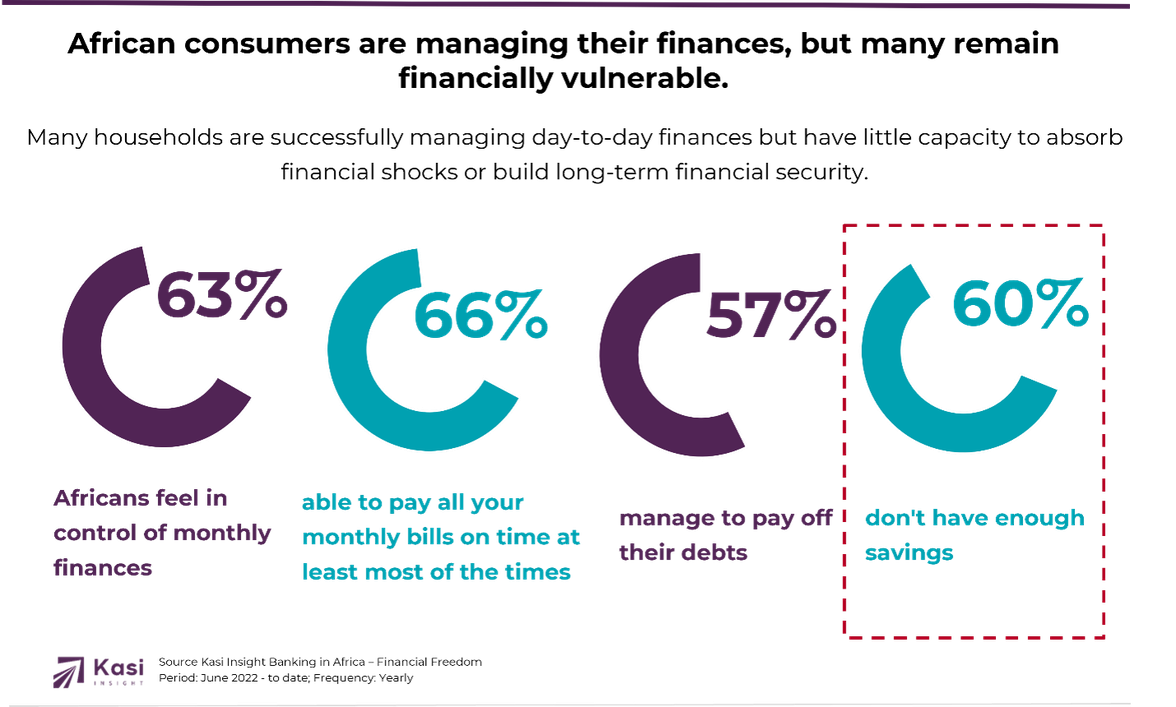

Consumers are becoming better money managers, but financial resilience remains out of reach.

Although consumers are adapting their financial behaviors, many remain financially vulnerable. Six in ten consumers say they do not have enough money in savings, while fewer than half believe they have sufficient savings to deal with unexpected expenses over the coming months.

Debt continues to place pressure on many households, even though the proportion of consumers struggling with repayments has gradually declined. More than four in ten consumers still report difficulties managing personal loans, business loans or credit obligations, indicating that financial stress remains widespread.

At the same time, consumers are demonstrating stronger financial discipline. Nearly two-thirds say they have a good handle on their monthly expenses, and most report paying their household bills on time either always or most of the time. These behaviors reflect households making increasingly deliberate financial decisions in response to constrained economic conditions.

Yet improved money management has not translated into greater financial comfort. Fewer than half of consumers believe they can currently afford the lifestyle they want, suggesting many are managing their finances more effectively because they have no alternative. African consumers are becoming better financial managers, but they are doing so within increasingly tight financial constraints.

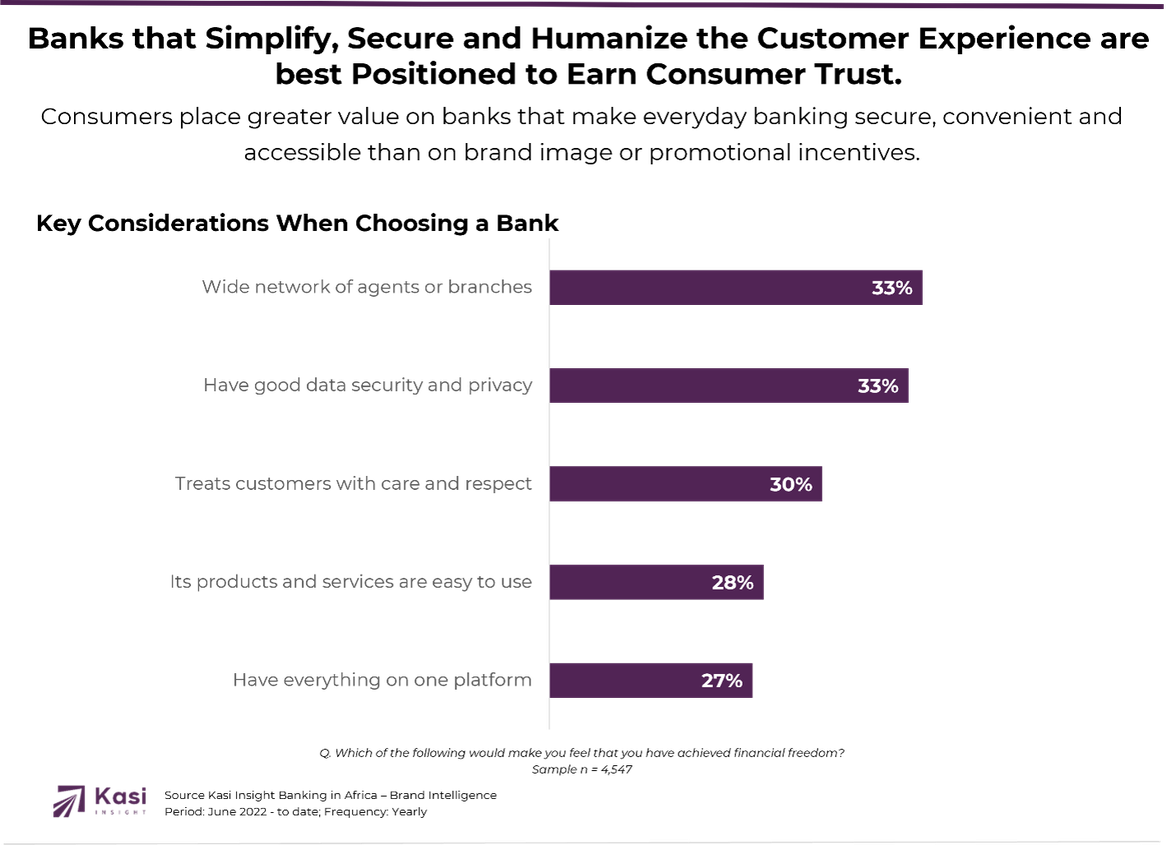

The banks that help customers build resilience, not just access money, will earn the next generation of trust.

As consumers' financial priorities evolve, so do their expectations of financial institutions. Trust is increasingly built through practical value rather than brand reputation alone. Consumers are looking for banks that simplify financial management, protect their money, provide reliable customer support and help them make progress towards their financial goals.

The strongest drivers of bank choice reflect these expectations. Consumers value institutions with accessible branch and agent networks, secure digital platforms, easy-to-use products, integrated financial services and a genuine commitment to helping customers achieve their financial ambitions. Affordability and customer experience remain important, but they are increasingly viewed as part of a broader expectation that banks should actively improve customers' financial wellbeing.

At the same time, consumers are embracing a broader financial ecosystem. Adoption of mobile money, digital banking, investment accounts and other financial services continues to grow, demonstrating that consumers are increasingly comfortable managing their finances across multiple platforms. Traditional banks are therefore competing not only with one another, but also with fintechs and digital-first providers offering greater convenience and flexibility.

For banks, the opportunity in the second half of 2026 extends beyond expanding product portfolios. Consumers are looking for partners that help them build emergency savings, manage debt responsibly, improve budgeting, track financial goals and prepare for future financial shocks. Institutions that position themselves around financial resilience rather than financial transactions will be best placed to deepen trust, strengthen customer loyalty and capture long-term growth.

The institutions that earn lasting trust will be those that help customers build resilience, make steady financial progress and navigate uncertainty with confidence. By aligning products, services and customer experiences with consumers' changing priorities, banks have an opportunity to become indispensable partners in Africa's journey towards financial freedom.

Understanding these changing priorities requires continuous consumer intelligence. Kasi Insight helps banks and financial institutions track evolving financial behaviors, measure consumer sentiment and uncover growth opportunities across Africa, enabling better product innovation, stronger customer relationships and more informed strategic decisions.

About Kasi Insight

Kasi Insight is Africa's leading decision intelligence firm specializing in high-frequency consumer and economic data across Africa. Through its proprietary survey infrastructure and analytics platform, Kasi provides real-time insights that help organizations anticipate economic shifts, understand consumer behavior, and make better strategic decisions.

We welcome collaboration with:

Organizations interested in exploring partnerships or accessing Kasi datasets are invited to contact our research team.

📧 yannick@kasiinsight.com

9 views

Share article

H1 2026 exposed the rise of the optimisation economy, with consumers actively reallocating spending rather than simply cutting back.

Africa's Consumer Confidence Slips Back Into Negative Territory in May

Assessment Of the Potential for Trade and Investment Exchanges Between Quebec and Africa