Alison Okatch

June 29, 2026

Share article

For much of the past years, conversations about consumers have focused on financial pressure and declining purchasing power. Yet the data suggests a more nuanced reality. African consumers are not simply buying less. Instead, they are rebuilding their shopping baskets around value, necessity and practicality.

The analysis in this report draws on Kasi Consumer Basket data, collected over 3 years, providing a longitudinal view of how household purchasing behavior has evolved across Africa. The data examines consumer preferences, brand choice drivers, shopping channels, product purchases, and usage patterns across key household categories, offering a comprehensive view of the typical African household basket and how it is being reshaped by changing economic conditions.

Inflation has not shrunk the African shopping basket; it has redesigned it. Across Kenya, Nigeria and South Africa, consumers are becoming more selective about what they buy, where they shop and which brands earn a place in their basket.

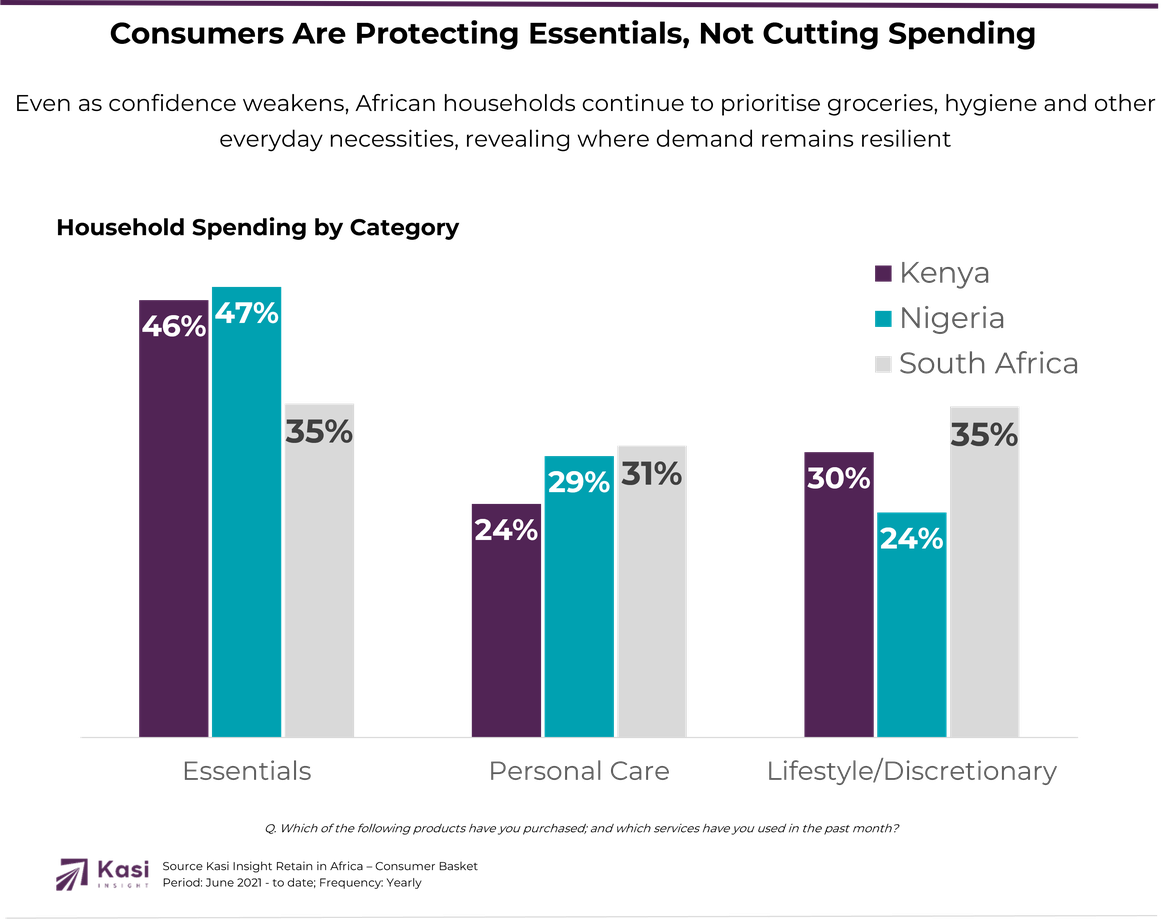

A closer look at recent purchases reveals how consumers are actively reshaping their spending priorities. In both Kenya and Nigeria, nearly half of all purchases fall within essential categories such as groceries, fresh produce, household cleaning products, personal hygiene items and airtime. These categories account for 46% and 47% of purchases respectively, compared to 35% in South Africa.

While discretionary spending remains present, particularly in South Africa where lifestyle purchases account for 35% of purchases, consumers are clearly prioritising products that support daily living. The data suggests that inflation has not eliminated spending; rather, it has concentrated spending around categories that households view as essential, useful and difficult to forgo. Consumers are becoming more selective, protecting necessities first before allocating remaining budgets to lifestyle and discretionary purchases.

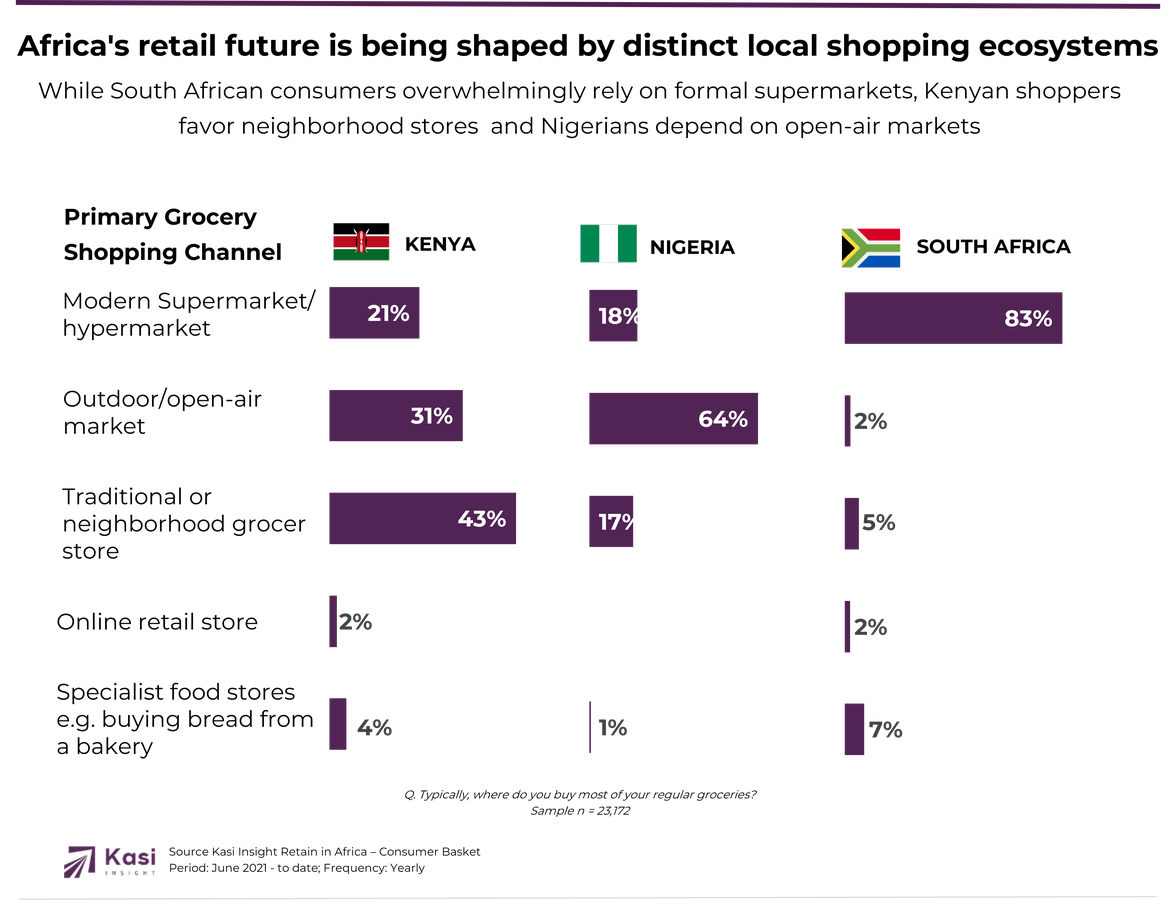

Africa's grocery landscape is far from uniform: success requires channel-specific strategies, with brands needing to win in neighborhood stores in Kenya, traditional markets in Nigeria, and modern retail in South Africa.

In Kenya, neighbourhood grocers have become the dominant grocery channel, accounting for 43% of regular grocery purchases. Their appeal extends beyond affordability. Convenience, accessibility and the ability to buy in smaller quantities make them well suited to households managing tight and unpredictable budgets.

In Nigeria, open-air markets remain the primary grocery destination, serving nearly two-thirds of consumers. These markets provide shoppers with greater flexibility and price transparency, allowing them to compare options and closely manage spending in an environment where food inflation continues to shape purchasing behaviour.

South Africa presents a different picture. Modern supermarkets and hypermarkets remain the dominant channel, accounting for more than 80% of grocery purchases. Here, consumers are increasingly focused on planned shopping, promotions and value comparisons as they seek to maximise household budgets within formal retail environments. Different channels, same objective: stretching every shopping trip further.

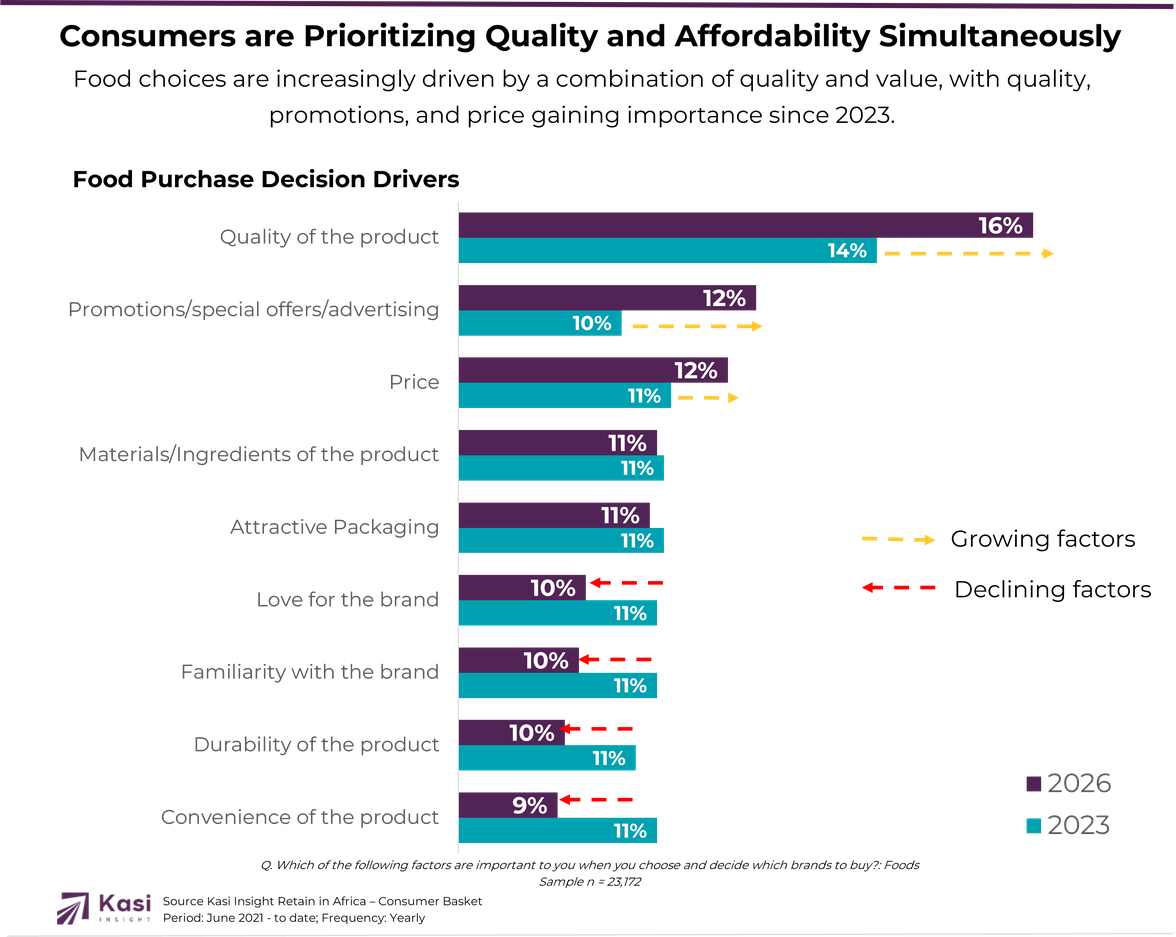

One of the clearest shifts emerging from the data is the changing role of brand loyalty. Across the region, traditional drivers such as familiarity and emotional attachment to brands have become less influential than they were just a few years ago. At the same time, practical considerations are gaining importance.

For food purchases, quality has become the most important purchase driver, increasing significantly between 2023 and 2026. At the same time, price and promotions have grown in importance, while traditional drivers such as familiarity and emotional attachment to brands have become less influential.

This suggests that consumers are not abandoning brands altogether. Rather, they are becoming more demanding. Brands must now earn their place in the basket through a clear value proposition. Consumers still want quality products, but they are increasingly unwilling to pay a premium for familiarity alone.

The result is a consumer who is less loyal but more intentional, constantly weighing quality against affordability before making a purchase.

The evidence from Kenya, Nigeria and South Africa points to a fundamental shift in consumer behaviour. Households are not simply cutting back; they are becoming more strategic.

Consumers are prioritising quality while demanding affordability. They are protecting spending on essential categories while making careful trade-offs elsewhere. They are embracing both formal and informal retail channels, using each where it delivers the greatest value.

The new African shopping basket is therefore not defined by scarcity. It is defined by optimisation. And for brands and retailers, success will increasingly depend on understanding how consumers are reallocating, not reducing, their spending.

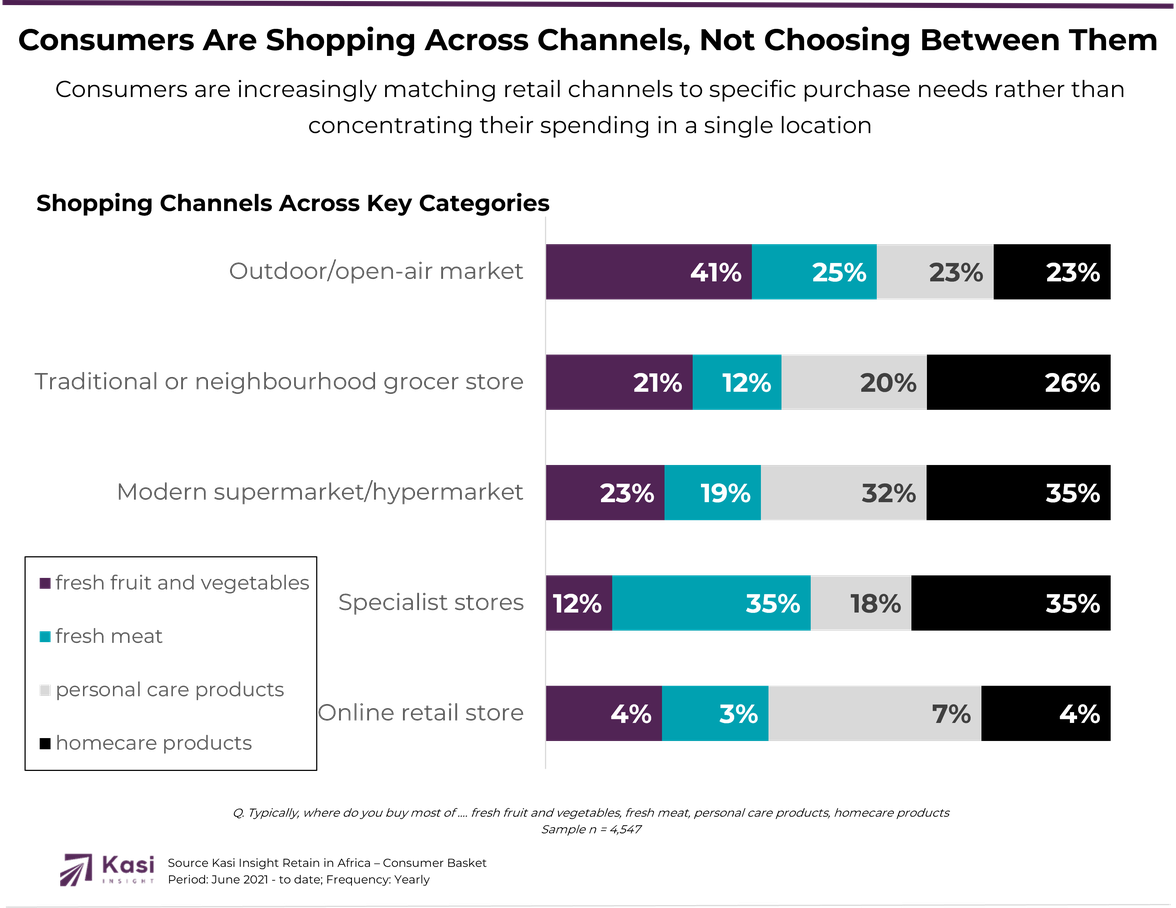

The most important lesson from the data is that African consumers are not choosing between formal and informal retail. They are choosing both.

Supermarkets continue to play a critical role in categories such as homecare, personal care and packaged goods. Markets, neighbourhood stores and specialist retailers remain essential for fresh foods and day-to-day replenishment purchases.

As a result, the consumer journey is becoming increasingly hybrid. A single household may buy vegetables from a market, meat from a butcher, cleaning products from a supermarket and personal care items from a specialist store, all within the same week. This behaviour reflects a highly sophisticated consumer who is constantly optimising value across multiple retail channels.

As we move into H2 2026, brands must recognise that consumers are not simply spending less, they are spending more strategically. Winning will depend on delivering quality, value and relevance across the channels and categories that matter most.

Talk to Kasi Insight about how consumer intelligence can help you stay ahead of Africa's changing shopping basket.

Kasi Insight is Africa's leading decision intelligence firm specializing in high-frequency consumer and economic data across Africa. Through its proprietary survey infrastructure and analytics platform, Kasi provides real-time insights that help organizations anticipate economic shifts, understand consumer behavior, and make better strategic decisions.

We welcome collaboration with:

Organizations interested in exploring partnerships or accessing Kasi datasets are invited to contact our research team.

📧 yannick@kasiinsight.com

8 views

Share article

African consumers have shifted from pursuing wealth to pursuing financial resilience, creating a new expectation that banks should help them build financial wellbeing

Africa's Consumer Confidence Slips Back Into Negative Territory in May

Assessment Of the Potential for Trade and Investment Exchanges Between Quebec and Africa